Given the market action in US equities generally and technology-related securities specifically, I suspect that many investors are quite concerned that a “major” bear market may be evolving, especially given the duration of the current equity bull market. US equities (S&P 500) have just today retested the previous lows established on October 29th.

But, what has changed? The macro environment hasn’t deteriorated in the past month, and may actually be improving. Just last week, Federal Reserve Vice Chair Clarida said the Fed was “close” to neutral, and they would need to be data dependent on further rate increases. That’s a significant shift from the more Hawkish tone that we’ve been hearing from other Federal Reserve members.

Furthermore, and most importantly, the economy continues to be provided with significant stimulus. I’ve highlighted the work from my former Invesco colleague, Charles DuBois, who has a very unique view of macro economics. He has shared the following with me:

As most of you know, since all spending = all income (an identity no one disagrees with), when the government is spending more than its income (a deficit), the private sector must be earning more than it is spending (a surplus), simply as a matter of accounting and as a point of logic.

As long as private debt creation is increasing, it provides a boost to the economy and profits. But when private debt creation turns down – look out as that is usually trouble – especially if the government’s deficit is declining at the same time.

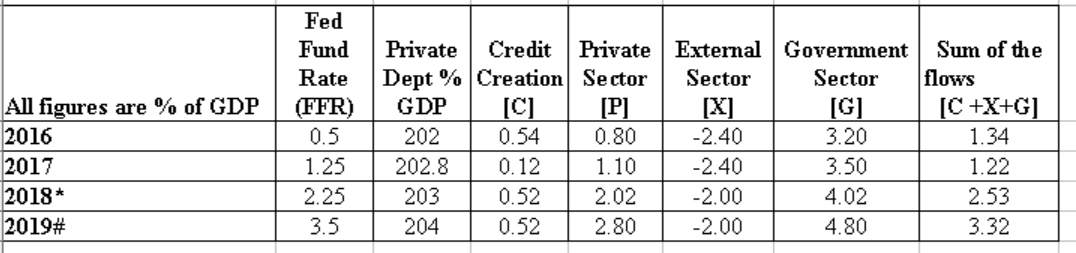

Basically, by taking the money created by government deficits and adding the money created by private credit (debt) creation and subtracting the outflow of money from the trade deficit – you get an excellent picture as to whether money is flowing into or out of the overall economy. If the latter, then a recession is likely around the corner.

On this score, the table on the “sectoral balances” is key. As long as the right hand column is reasonably positive, economic conditions should be OK. Right now money is flowing in – so the current market downdrafts should not develop into a major bear market. Separately, it is useful, as confirmation, to follow leading indicators of the economy – which are also in good shape.

The few economists, to my knowledge, who saw the 2008-09 collapse coming

were using this type of framework.

Over the long run, growth is a function of labor force growth and productivity.

On a more cyclical basis, growth is importantly related to money flows..

Thank you, Charles!

As a further point of reference, and according to Alan Longbon, “the US budget deficit is $100 billion in October 2018; this is a net expansion of income and savings in the private sector. The good news is that dollars are being added to the economy by the Federal government, allowing the private sector to post a $100 billion surplus.

Private credit growth has rebounded this month and made a $17B contribution to aggregate demand and fiscal flows.”