I had the distinct pleasure to once again participate in the IFEBP annual conference. This event had me traveling to New Orleans where it was incredibly warm and humid. There were times during the trip that had me feeling as if I were in a frying pan. Ironically, public pension systems should be feeling the heat at this time, too, as allocations to equity-like products now represent about 70% of the average portfolio which is up more than 30% from just a couple of decades ago.

My presentation was on the “Key Factors in the Long-term Sustainability of Defined Benefit Plans”, and one of the points that I was making is the fact that public pension sponsors and their consultants are injecting a ton more risk into their asset allocation in an attempt to achieve the “Holy Grail”, I mean the return on asset assumption (ROA).

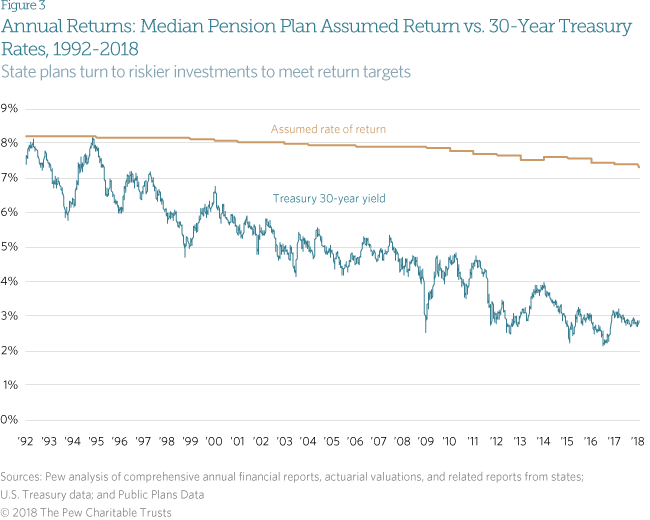

Twenty years ago, states needed only to exceed the yield on a 30-year Treasury bond by 1% in order to meet their investment targets. Currently, the typical state would need to outperform a 30-year Treasury bond by nearly 4.5% to meet its now-lower investment assumption. That reality has forced plans to take on higher levels of investment risk and at a time when U.S. equity markets have enjoyed a historic bull market run.

KCS and Ryan ALM have been encouraging plans to take a different path at this time. We want plans to get their arms around the plan’s specific liabilities and to use that output to drive investment structure and asset allocation decisions. We believe that DB plans need to be sustained, but doing the same old, same old in this environment will prove devastating to funding levels once the next correction occurs.

Sponsors needed to be thinking about this strategy in 2006 and not in 2009 after the market collapsed. Well, are you thinking about de-risking your plan now? If not, why not? It might just be too late in another three to four years.