A colleague recently passed to me an interesting article from Forbes, titled “Is There A War Being Waged Against Older Workers In The Workplace?” The article raises a number of viable arguments in support of such a claim, including specific job screening criteria for candidates with 3-7 or 7-10 years of relevant experience. The article’s author contemplates the last time one saw a job opening posted for someone possessing 20-30 years of experience.

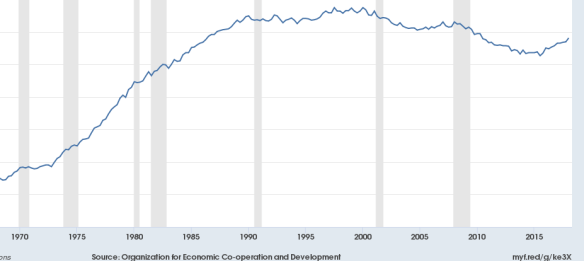

Based on the chart below it certainly appears that opportunities have weakened for workers aged 25-54 years-old.

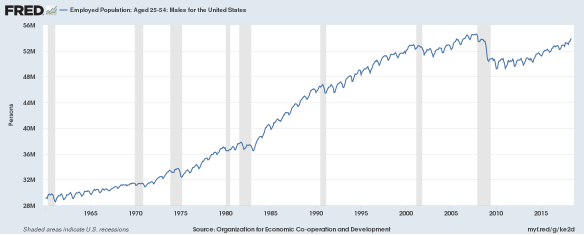

It is actually a bleaker picture if one focuses exclusively on the male population in that age category, as there are roughly 2 million fewer males 25-54 working today since the start of the GFC. I suspect that most of those former employees are not sitting on the sidelines because they are independently wealthy.

Given that focus, it leads companies to a population well south of 40 years-old and definitely neglects those viable candidates in the 40+-year-old category. What it also does is damage one’s ability to save for retirement, which is why I am particularly interested in this subject matter. As the private sector has moved from defined benefit to defined contribution retirement plans, the emphasis on funding and managing such a vehicle has fallen squarely on the shoulders of the employee, who in many cases have neither the financial resources nor the investment capability to handle this responsibility.

Given that individuals rarely save outside of an employer’s sponsored plan, losing a job in one’s 40s or 50s has a profound impact on that employee’s ability to generate a retirement balance that will help them live through retirement. Furthermore, it is often the case that older employees finally have other major expenses (children, house, college, etc.) behind them and they are counting on the last 15-20 years of employment to pad their retirement balances. The government even recognizes this phenomenon by allowing “catch-up” contributions into defined contribution accounts after age 50.

Regrettably, DC balances are often used as employment bridge loans (almost like an unemployment benefit) when a worker has been displaced. Given this scenario, contributions cease to be made, while balances weaken as opposed to growing through the benefits of compounding. For workers experiencing extended periods of unemployment, their ability to generate a retirement benefit is impaired tremendously.

We read the financial papers and listen to the rosy employment scenarios on the TV and radio, but don’t believe for one minute that our current labor conditions are appropriately captured in the published unemployment statistics. There are too many older Americans that have been displaced from the labor force whose prospects for reentry are slim, at best!