The great migration from defined benefit (DB) plans to defined contribution (DC) plans has been underway for roughly four decades within the private sector. How’s it working out for the millions of US workers hoping to retire one day? Will their “golden years” be bright and shiny or tarnished as a result of asking untrained individuals to fund, manage, and then disburse a “retirement” benefit with out the financial resources, skill, or crystal ball to accomplish the objective?

So, how are our DC participants doing? According to Alight’s recently released2023 Universe Benchmarksreport, NOT WELL! Among more than 3 million participants that were surveyed, the median balance of only $23,818 is at its lowest level in more than a decade. Sure, new participants are coming into the survey all the time and they tend to have shorter working histories and smaller balances, but before you believe that this is the primary reason for the meager balances, participants across all timelines suffered significant declines in 2022 as balances fell -14.7% on average.

In addition to reporting on the median account balances, Alight’s survey also pointed out that average participation and contribution rates declined. One in 5 of Alight’s participants had a loan outstanding, but that is down from a peak of nearly 30% about a decade ago. When looking at the average balance, which clearly favors those of higher incomes and longer tenures, 2022 wasn’t much better as the average balance fell $111,210 from $114,280 at the start of the year. For even those with more robust balances, relying on a balance of this size will unfortunately not produce a dignified retirement for the participant.

Let’s hope that the combination of the “Great Resignation” and the generation of pension income in 2022 will slow down the termination of more DB plans within the private sector. We, at Ryan ALM, believe that DB plans are an incredible retention tool. We also know that there are strategies (namely cash flow matching) that can secure the promised benefits at reasonable cost and with prudent risk, reducing the potential for negative shocks to the corporation’s income statement. US workers need our help if they are going to achieve the dream of a dignified retirement. Doing the same old, same old is not the right approach.

I recently produced the following on LinkedIn.com.

What PIVOT?

As we’ve been consistently saying, economies don’t roll into recessions with full employment and wage growth >4%. Recent economic releases continue to support the Fed’s aggressive rate increases with more likely to follow.

The US 2-year Treasury Note yield is back at 4.87% this morning. It is within 20 bps of the peak yield achieved earlier this year. Furthermore, it is up 110 bps since days following SVB’s collapse and the perceived end of the banking industry.

US interest rates are not high enough to thwart economic growth. If you were involved in our industry in the late ’70s and early ’80s you witnessed high double-digit rates.

There has perhaps never been a decade like the ’90s for investing in US equities – S&P 500 compounded at 18.5% for the decade. Yet, the 10-year Treasury yield averaged about 6.5% for that period ranging from a low of 4% (1998) to a high of 9.5% (1995). The 10-year US Treasury Note yield is ONLY 3.83% this morning, even after a 12 bps rise following the GDP upward revision. STOP looking at the movement from Covid-19 induced lows. Focus on the absolute level of US Treasuries at this time. It won’t cloud your judgment.

Following today’s release of ADP’s National Jobs Report (497,000 vs. 220,000 expectation), I produced a follow-up thought.

Interest rates are rising significantly this morning following the blowout jobs #. Just one more data point crushing the “pivot crowd”.

2-year Treasury Note yields are up 9 bps (as of 9:33 am) and sit at 5.04%. This is only 3 bps off the peak yield achieved earlier this year and 1.26% higher than the low achieved after SVB’s demise. US 10-year Treasury Note yield is back over 4% for the first time in months.

Good news: Higher yields are providing pension plan sponsors of all kinds (corp, public, and multiemployer) with the wonderful opportunity to significantly reduce risk by cash flow matching plan liabilities and assets at a very attractive Yield To Worst (YTW). Don’t let the markets dictate your funded status and contribution expenses. Take risk off the table today.

Happy Fourth of July! Thank you to all who have served our nation to provide us with the freedoms that we enjoy, but often take for granted.

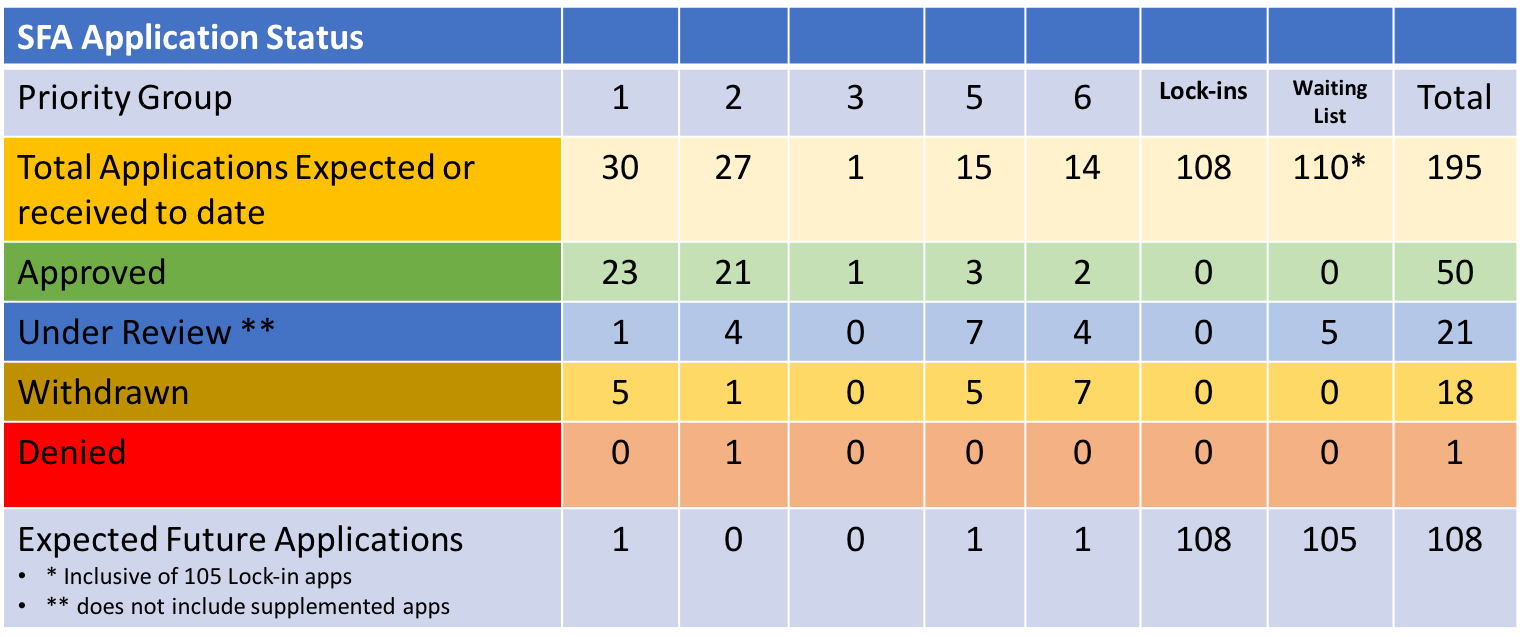

With respect to the PBGC’s implementation of the ARPA pension legislation, last week was quite busy, as five plans had their applications approved, including the first two Priority Group 6 members to get the SFA grant award. The National Integrated Group Pension Plan and the PACE Industry Union-Management Pension Plan will receive approximately $2.2 billion to cover their 112,776 participants.

The Composition Roofers No. 42 Pension Plan and the IBEW Local No. 237 Pension Plan, Priority Group 2 members, each had revised applications approved during the last 7 days. They will receive in total $65.9 million (including interest) for their 925 members. The last of the five approved applications was for supplemental proceeds for Priority Group 2 member Bricklayers and Allied Craftsmen Local 7 Pension Plan, which will get $9.4 million for its 397 pensioners.

In other news, three plans withdrew applications, presumably under the guidance of the PBGC. These plans, the Pension Plan of the Moving Picture Machine Operators Union Local 306 (PG 5), GCIU-Employer Retirement Benefit Plan (PG 6), and Local 210’s Pension Plan (PG 5), were seeking $944 million collectively, with a significant majority of those assets earmarked for the GCIU plan. GCIU’s application was their initial one, while the other two had already submitted revised applications. Perhaps three times will prove to be the charm.

There were no additions to either the waiting list or locked-in groupings. There still remain 110 waiting list candidates of which 108 have locked in their valuation date. As we begin the Fourth of July celebrations, we should also celebrate the fact that 50 multiemployer plans have received critical funding to help meet the promises that were given to their plan participants.

Q: Should a pension plan with a 90% funded status have the same asset allocation as a 60% funded plan?

A: NO! Asset allocation should be based on the economic funded status.

Many asset allocation models are based on achieving a target return (ROA) and ignore the funded status. This has been a critical mistake as best demonstrated by what has happened since 1999. In the 1990s, most pensions had a growing surplus. Instead of reacting to this funded status, most pensions focused on achieving a then target ROA of around 8.00%. During the 1990s, asset allocation models increased their weight for equities and reduced their weight toward fixed income to the lowest level ever as interest rates continued a secular decline. By the end of 1999, it was common to see an allocation of 75%+ to equities.

When the equity correction came in 2000, it hit the funded status hard. Ryan ALM estimates that the S&P 500 underperformed economic liability growth by over 60% during the 2000 – 2002 equity correction. As a result, the funded status went from a nice surplus to a sizeable deficit. This reality caused a spike in contribution costs. For many pensions, contribution costs went up over 300% in those three years and they have continued to spike through today. Contributions for many pensions are now over 10x higher today than in fiscal 1999. This is the pension crisis I outlined in my 2013 book “The U.S. Pension Crisis”. This increased contribution cost led numerous corporations to freeze and terminate their defined benefit plan through a pension risk transfer (PRT). This may be the worst outcome for new employees who were given a less secure defined contribution plan instead.

There are several lessons to be learned from the 2000-02 equity correction:

True Economic Objective – is to secure benefits in a cost-efficient manner with prudent risk… it is not a return objective.

It’s All about Cash Flows – the goal is to have asset cash flows match or exceed liability cash flows with certainty. This should be the quest of any pension. This is best accomplished with a cash flow matching strategy using bonds. It used to be called Dedication and Defeasance.

Actuarial Projections – the actuarial projections of benefits and expenses or liability cash flows should be the focus of asset cash flows. Too often such actuarial projections are not provided in the annual actuarial report. It is critical that pension assets know what they are funding. As a result, actuarial projections should be mandated by the plan sponsor, so consultants and asset liability managers know the liability cash flows they need to fund.

Economic Funded Status – actuaries have a tough and tedious job given all the calculations they need to create. As a result, they tend to publish their actuarial report annually several months after the end of the fiscal year. It is hard, if not impossible, for assets to function efficiently if their objective is only known annually several months delinquent. As a solution, the Ryan team developed the Custom Liability Index (CLI) as the proper benchmark for any pension providing all of the calculations and data needed for plan sponsors, consultants and asset liability managers to perform their duties effectively. The CLI will calculate the market value of liabilities so the economic funded status can be determined when compared to the market value of assets. This economic funded status should be the focus of asset allocation.

Asset Allocation – should be responsive to the funded status. As the funded ratio improves, a greater allocation to cash flow matching with bonds should be enacted. Any pension fully funded should consider a high cash flow matching allocation. Utopia is to have risky assets in the surplus portfolio and not the asset liability portfolio. Had pensions done this in the late 1990s there would not have been the contribution cost spikes pensions suffered ever since.

“Common sense is not common. It requires preferred sense”.

We hope that your week has begun well. Sorry for the delay in getting our weekly ARPA update out. Three cancelled planes, flights supposedly from 4 different airports, an Amtrak train, and numerous Uber rides, and I finally made it to Orlando, FL for the FPPTA conference. What a journey. Travel in the summer is far worse than trying to get around in the winter.

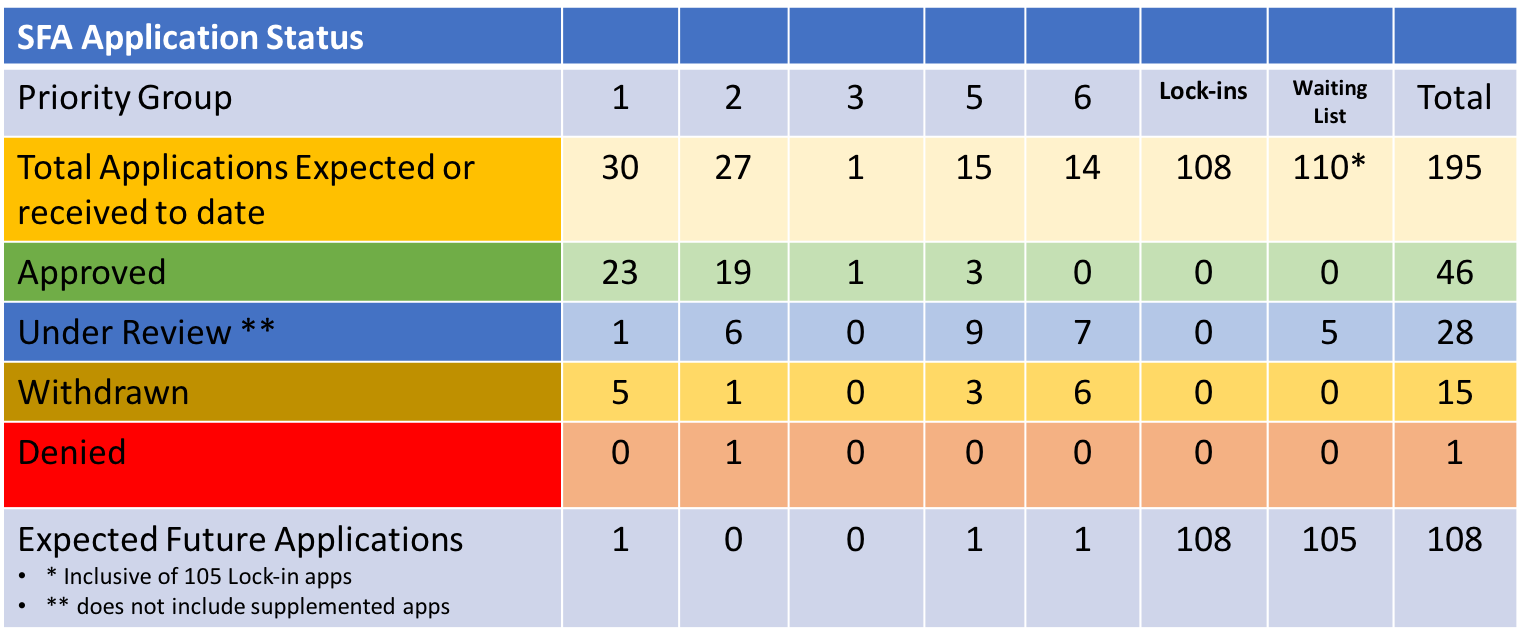

Well, the wait might not have been worth it, as there is very little activity to report from last week. According to the PBGC’s website, there were no new applications filed or approved, and none denied. There were two initial applications withdrawn. Both had been filed on March 10, 2023. The Southern California United Food and Commercial Workers Unions and Food Employers Joint Pension Plan (UFCW), a Priority Group 6 plan, is seeking nearly $1.2 billion in Special Financial Assistance (SFA) for its 193,302 plan participants. They withdrew their application on June 21st. The Union de Tronquistas de Puerto Rico Local 901 Pension Plan, a Priority Group 1 plan (insolvency), is seeking $38.6 million for the 4,029 members of the plan. They withdrew their application on June 23rd.

There were no new additions to the waitlist, which continues to have 110 members. Of those 110, all but two funds have locked in valuation dates. According to the PBGC’s website, the e-filing portal is temporarily closed, but plans “plans may request to be placed on the waiting list in accordance with the instructions in PBGC guidance.”

As of last week, five of the 110 funds residing on the waitlist had submitted applications to the PBGC. Those plans included, Laborers’ International Union of North America Local Union No. 1822 Pension Fund, Teamsters Local 11’s Pension Plan, UFCW Regional Pension Fund, IUE-CWA Pension Plan, and the Newspaper Guild International Pension Plan. I believe that the PBGC has 120 days to approve or reject the applications which has been the operating procedure for priority group plans (1-6).

We encourage any multiemployer plan going through the process of receiving and investing the SFA to reach out to us for guidance. Cash Flow Matching is the most appropriate investment strategy, as the segregated SFA proceeds represent a sinking fund designed to pay benefits and expenses as far into the future as the allocation will go. Minimizing volatility of the corpus is critically important to ensuring the success of this program.

We understand that US public pension systems operate under different accounting standards (GASB) than those sponsored by private companies (FASB), but should those differences create asset allocation frameworks that differ so widely from those of corporate plans? Furthermore, those differences create much greater uncertainty, as the public fund’s larger exposure to equities and equity-like alternatives magnify the annual contribution and funded status volatility. Just how different are they?

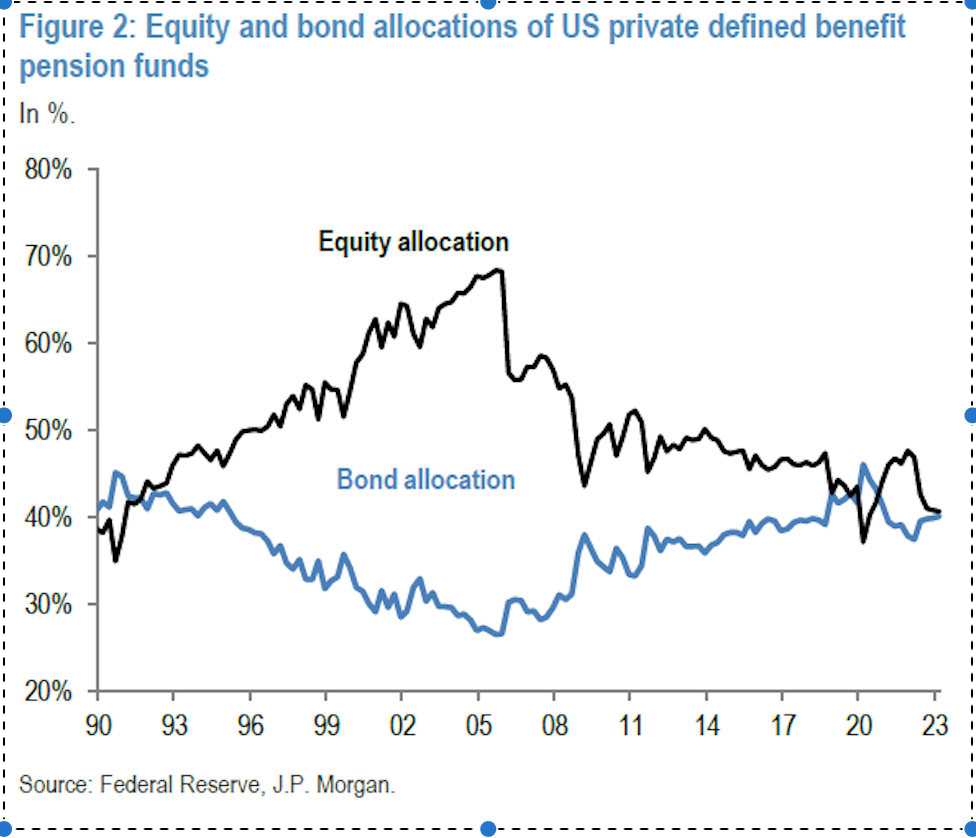

The first graph highlights the asset allocation for US private plans from 1990 into 2023.

As one can see, equity exposure grew steadily from the 1990s into 2007, before falling rapidly until today, where equity exposure mirrors the bond allocation. Some of that movement was driven by the tremendous returns achieved during the go-go ’90s, followed by the collapse of those markets in 2008. Today’s allocation is mostly driven by a desire to stabilize the funded status (and contribution expenses) for either a possible pension risk transfer (PRT) or minimization of PBGC premium expenses, or both.

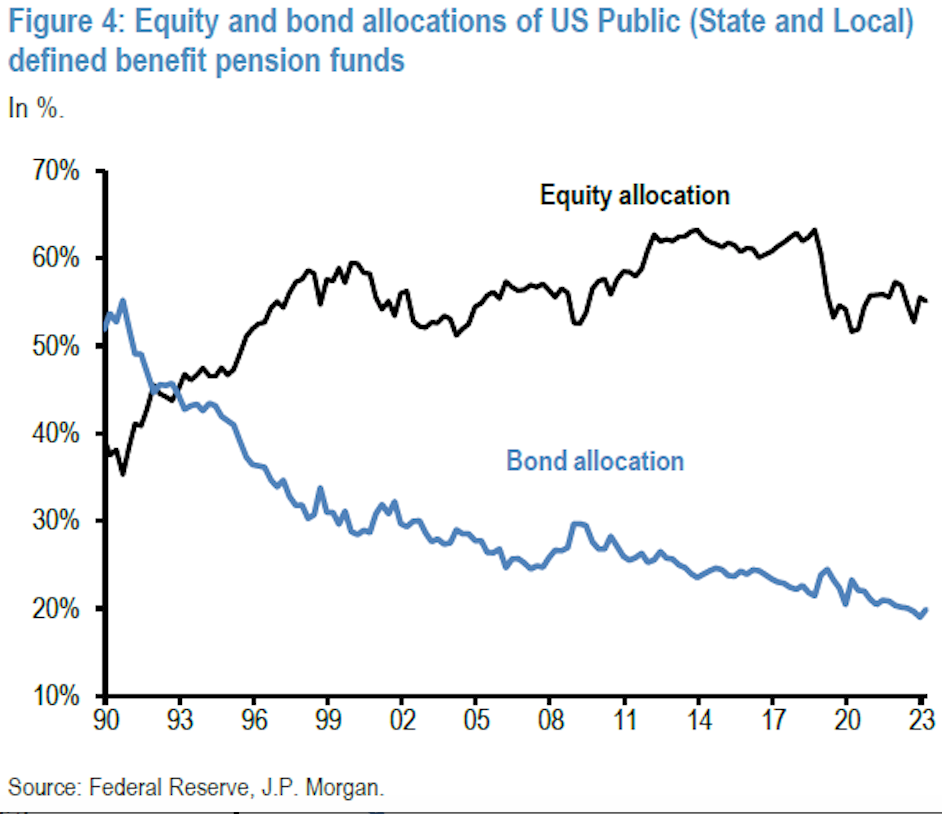

On the other hand, public funds which started at very similar equity exposure in 1990, have adopted a much more aggressive, almost let-it-ride mentality. As the graph below reveals, equity exposure resides in the mid-50% range or about 15% above that of private pensions. At the same time, exposure to bonds has plummeted declining more than 60%, as alternative investments have taken on a greater role. Has this shift improved funding?

Both private and public plans had the opportunity to significantly reduce the volatility around the funded status back in 1999, following the historic equity market. Both sets of pension funds were overfunded on average, but neither plan type took advantage of their favorable funded status to SECURE the promised benefits by defeasing the pension promises. As a result, both asset bases became victims to two incredible bear market events – 2000 to 2002 and 2007 to 2009. Since the devastating Great Financial Crisis, corporate America has steadily reduced exposure to equities, while increasing bond exposure. As a result, the fund status for the average private fund is presently at 99.3% and the funding deficit is only $8.9 billion as of December 31, 2022, for the largest 100 plans (according to Milliman’s 2023 annual study). Finally, the discount rate is 5.18%.

On the other hand, public pension funding continues to be incredibly volatile. According to Milliman and their 2023 public fund report on the largest 100 public pension systems, the aggregate funded ratio has fallen to 72.6%, erasing the market gains experienced in 2020 and 2021. Furthermore, the 2022 market underperformance has widened the funding gap between plan assets and liabilities to a new high of $1.63 trillion as of December 31, 2022. The discount rate is in most cases equivalent to the plan’s return on asset assumption (ROA) of roughly 7%, or 1.82% higher than that of private plans. This suggests that if public pension plans would mark to market their liabilities using ASC 715 discount rates (AA corporate bonds) the present value of their liabilities would increase by 18% to 27% (discount rate difference of 1.82% x duration of liabilities (10 to 15 years))… and their economic funded ratio would decline from 72.6% to between 57.2% to 61.5%.

As US interest rates rise, the new investing environment is providing pension America with a second opportunity to substantially reduce risk which will help to stabilize the funded status and contribution expenses, while buying time for the equity and equity-like exposure to grow unencumbered. Will plan sponsors take advantage of this new paradigm, or will we continue to witness significant market volatility whipsaw the funded status and contribution expenses for primarily public plans?

We suggest that public pension systems adopt an asset allocation that resembles private plans. Increase the allocation to fixed income, especially now that an investment-grade corporate bond portfolio’s YTW can earn roughly 78% of the ROA with little risk. Use the bond allocation to defease your plan’s near-term Retired Lives Liabilities chronologically which will improve liquidity, while also stabilizing the funded status for that portion of the portfolio that is now carefully matched to the plan’s liabilities. By buying time, the equity and alternative exposure can grow unencumbered and be used to meet future liability growth.

Pension systems need to be protected and preserved. Continuing to ride the asset allocation rollercoaster is not the way to protect plans. Adopt a greater focus on risk reduction and securing the plan’s promises and preservation of these incredibly important vehicles will be more easily achieved.

On October 11, 2022, I penned a blog post titled “Rates Aren’t High Yet, But They Might Get There“, in which I highlighted the fact that the 3-year Treasury yield was trading at 4.33%, the highest rate along the Treasury yield curve. I also showed that rates during the 1990s were substantially higher and that economic growth was not stalled given those higher US interest rates, as the GDP averaged more than 3.5% annualized growth.

I forecasted in the post that US interest rates at that level were not going to curtail economic growth despite the perception by many in the markets that a recession was around the corner which would lead to a Fed pivot and falling rates sooner rather than later. Not surprisingly, they haven’t! The yield on the US 3-year Treasury Note at 4.33% today is exactly where it was 7+ months ago. However, the 3-year yield is not the highest along the Treasury curve, as yields for the 1-month bills to 2-year notes are all substantially higher, with the 6-month Treasury Bill trading at a 5.41% yield (2:27 pm).

So, rates, at least on the short end of the curve have risen dramatically, with no pivot in sight! Yet, economic growth has been sustained with forecasts of 1.9% annualized growth (for Q2’23) according to the Atlanta Fed’s GDPNow modeling. That doesn’t seem recessionary. Nor does the fact that the US labor market does not show signs of cracking despite higher US rates. Yes, inflation has moderated from the peak observed last summer, but we have a long way to go until the Fed’s target of 2% has been achieved.

In testimony before Congress this morning, Fed Chairman Powell stated that most Fed Governors anticipated further interest rate increases before the end of 2023. Again, no great pivot in the forecast. Despite the higher rates, US home builders seem immune, as groundbreaking on U.S. single-family homebuilding projects surged in May by the most in more than three decades, while permits for future construction also climbed. So much for the impact of higher rates.

I’ve mentioned in many posts that I thought the investment community was anchored into believing that rates and inflation would always be low, as most participants had only experienced low levels during their careers. Furthermore, the US Federal Reserve would always be there to step into the fray when the investment environment became “messy”. We cautioned everyone not to be complacent. Each of the Ryan ALM senior fixed-income team members was in the industry during the last inflationary cycle. We know what it is like to experience rapidly rising rates in an attempt to thwart inflation. You don’t want to fight the Fed, yet that is what our current investing community has done throughout the last 15 months.

Back in October, we warned you that rates were likely to climb and that the level of rates at that time would not lead to a recession in the near future. The Federal Funds Rate currently stands at 5%-5.25% with the likelihood of rates continuing to rise. This is exceptional news for pension plan sponsors and retirees, as the cash flows from bonds can now support risk-reducing strategies that don’t force one to take unnecessary risks. Use this environment to take risks off the table. Rates are likely to rise, inflation is not likely to plummet to 2% anytime soon, the economy is not going to collapse, and the Fed is in control. Don’t ignore the Fed.

Good morning. We are pleased to provide you with the latest update on the progress of the PBGC’s implementation of the ARPA legislation.

Last week proved to be a quiet one for the agency and the multiemployer plans seeking Special Financial Assistance (SFA). There were no new applications submitted for review and none were approved from among the many still residing with the PBGC. However, Local 996 Pension Plan did receive the proceeds from its supplemental application that awarded them $8.6 million to further support the promised benefits for the 2,356 plan participants. This is on top of the $54.1 million that was received in December 2022 following the submission of the revised SFA application.

There weren’t any applications denied during the previous week. In addition, there were no new pension plans added to the PBGC’s waitlist or plans securing a valuation date. There were three plans that withdrew applications during the last 7 days. They include the Bakery and Confectionery Union and Industry International Pension Fund, Laborers National Pension Fund, and Southwestern Pennsylvania and Western Maryland Area Teamsters and Employers Pension Fund. The Southwestern plan is a Priority Group 5 system, while the other two are categorized as Priority Group 6 members. Each plan had filed its initial application. In total, they are seeking $4.2 billion for nearly 150,000 participants. The majority of the SFA would go to the Bakery and Confectionery Union ($3.8 billion).

Bonds are, perhaps, the only asset class with the certainty of their cash flows.

You know with near certainty (excluding any defaults) the semi-annual interest payments and the principal payment at maturity (for non-callable bonds). That is why non-callable bonds have a long and proven history of being chosen as the proper fit to defease and cash flow match liability cash flows.

Ryan ALM urges pensions, OPEBs, and any other asset base with a liability-driven objective to use bonds for their intrinsic value. We do not view or recommend bonds as performance vehicles even though they can certainly outperform other asset classes when interest rates are going down as a secular trend (i.e. 1982 – 2021). We urge asset allocation models to separate liquidity (cash flow) assets from growth (alpha) assets. Use bonds as your liquidity assets to match and fund liability cash flows chronologically… especially with today’s inverse yield curve. This will BUY TIME for the alpha assets to grow unencumbered. Importantly, this will eliminate the CASH SWEEP of other asset classes that reduce their total returns (ROA). According to a Guinness Asset Management study, about 50% of the S&P 500 10-year rolling average returns since 1940 come from dividends and the reinvestment of those dividends.

Since contributions are the first source to fund benefits and expenses (B+E), current assets need to fund NET liability cash flows. For many pensions, contribution costs are large so net liabilities are a much less onerous cash flow to fund. In many pensions, just a 15% allocation to bonds can fund 1-7 years of B+E. This is a better use for bonds than any performance target. The longer the period funded by bonds, the greater the probability of achieving high rates of returns on the growth assets. Liquidity and growth assets should be a synergistic team that when working together achieves the cash flow requirements and the ROA target and SECURES the promised benefits.

We haven’t had an interest rate environment as positive as this in a long time. Use the higher rates to your advantage by taking risks off the table through a defeasement strategy. Everyone will sleep much better.

We, at Ryan ALM, believe that Risk is best defined as the uncertainty of achieving the objective. Any argument? What is the primary objective of managing a pension plan? Again, we believe that it is the funding and SECURING of the promised benefits in a cost-efficient manner and with prudent risk. The only reason that defined benefit pension plans exist is to pre-fund promised retirement benefits. Regrettably, our industry, at least for public and multiemployer plans, has adopted a very different primary objective… one that is focused on achieving a return on asset objective (ROA).

With a return focus, great uncertainty is introduced into the process. So if risk is defined as the uncertainty of achieving the objective, why would one want to adopt a strategy that only serves to create greater uncertainty? When pension systems were first introduced many decades ago, they were often managed in a similar fashion to insurance companies and lottery systems that took a present value (PV) calculation of the future promised benefits (FV) and funded the plan accordingly, and usually thru a cash flow matching strategy or defeasement. There was no need to subject precious fund assets to the whims of the market. There was no forecasting of asset class performance based on a historical perspective that might be achieved at some point in the future. No games!

Has the changing of the primary objective/focus led to better outcomes? Absolutely, not. As a result of all the volatility associated with a return focus, pension plan sponsors are saddled with greater contribution expenses, a more volatile funded status, the introduction of much more complicated products/structures, less liquidity, and far greater uncertainty as to the sustainability of these critically important plans.

Despite all this, there is some good news. After nearly four decades of falling US interest rates that created a bunch of unintended consequences, the current US interest rate environment is once again very positive for pension systems. Not only are allocations to fixed income producing wonderful cash flow, but the PV of pension liabilities is falling, too. With only a modest change in the asset allocation approach, one could significantly reduce the uncertainty of achieving the primary objective of securing the promised benefits at both a reasonable cost and with prudent risk.

Migrate your current core fixed income from a return-seeking focus to one that uses the fixed income cash flows to secure the promised benefits through a cash flow matching defeasement strategy. Your plan’s assets and liabilities will move in lock-step with one another for that portion of the plan that is defeased. Now that is certainty! Don’t continue to just ride the asset allocation rollercoaster hoping to achieve a ROA objective.