By: Russ Kamp, Managing Director, Ryan ALM, Inc.

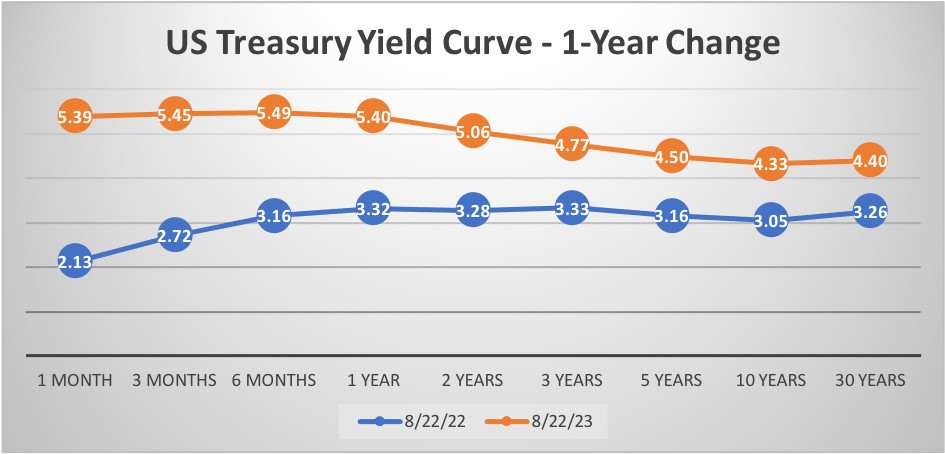

August 2023, proved to be another challenging month for return-seeking fixed income managers and their strategies when using the BB Aggregate index as the proxy, as the index declined -4% (-3.98% if you want exactness). This was the most challenging monthly result so far in 2023. For the year-to-date period, the index has posted a 1.4% return, as the higher yields buffered the loss of principal value as US interest rates continued their path upward.

How are things shaping up for the balance of the year? Well, we at Ryan ALM, Inc. are not in the business of predicting US interest rates, but we do look at the data like most everyone else. What we see is a nearly historic labor market, rising oil prices, with WTI now over $87/barrel, and a GDP for Q3’23 of 5.6% according to the Atlanta Fed’s GDPNow model (as of 9/1/23), which would certainly suggest that a recession is not in our immediate future. Given these metrics, is there really any wonder where US rates might be headed?

As you may recall, we railed against the use of return-seeking fixed income strategies as investment vehicles for the Special Financial Assistance (SFA) received by multiemployer plans under ARPA. We spoke and wrote frequently that rising US interest rates would negatively impact the total return for traditional fixed income strategies… and they have! As a reminder, 2022 was the worst year, by far, for the BB Aggregate index as it posted a -13% return. 2023 is not nearly as bad, but it certainly isn’t helping preserve the SFA which is supposed to be used to secure benefits and expenses far into the future.

We also discussed the importance of the sequencing of returns. Witness dramatic losses, such as those incurred last year, early in the life of the SFA and you create a situation where the benefit “coverage” period is shortened, and perhaps dramatically so. For those plans still waiting (hoping) to receive SFA support, don’t play games with the funds. Use those proceeds to SECURE as many benefits and expenses as far into the future as possible (as the ARPA legislation requires). Remember, when you defease pension liabilities through a Cash Flow Matching (CFM) strategy, you are matching future value liabilities that aren’t interest rate sensitive, which remains the biggest risk in the management of bonds.