By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Americans nearing retirement are in most cases unprepared for the hopefully next 20-25 or more years. Sure, there is Social Security (thank goodness), but the average monthly SS payment is only $1,827 or $21,924 per year. When you figure that the average rent for an apartment is $1,372 per an August 2023 review by Apartment List, that doesn’t give the SS recipient a lot of disposable income. In addition to housing costs, Seniors need to be concerned about healthcare costs that tend to dominate expenditures during one’s later years. There are obviously many other regular expenditures, including food, transportation, clothing, etc.

According to the Bureau of Labor Statistics, the “average” 65-year-old had an annual expenditure of $57,818 as of 2022. What is the median average income for Americans of a similar age? Unfortunately, it is only $50,290 (U.S. Census Bureau), including SS and any and all retirement accounts (DB, DC, IRA, ). So, before the year even begins, the average American 65-year-old or older is behind the 8 ball by more than $7,500, and that is before the potential extraordinary expense that could further sabotage one’s retirement.

This is bad, and the story is getting worse. According to Benzinga, the average American retiree had <$171,000 in retirement savings, but 37% of Americans have saved nothing for retirement, which is an increase of 7% just since 2022. In addition, 71% of Americans are carrying non-mortgage debt in retirement of just under $20,000. Student loan debt (Parent Plus Loans) and medical expenditures are contributing to this burgeoning total. In many cases the lack of retirement resources has been the result of an early retirement brought about because of a disability rendering the possibility of working beyond 65 a moot point.

Again, asking employees with little discretionary income, no or little investment acumen, and a cloudy crystal ball to help with planning until one’s demise makes the use of defined contribution plans a silly alternative to traditional defined benefit plans as one’s primary retirement plan. As an FYI, my Mom and Dad have lived on my Dad’s small DB monthly payout ($1,400ish), Social Security, and a little savings for 32+ years. They have never been wealthy, but they’ve been secure in knowing that that check will arrive every month. My Dad is now 94. I can’t imagine that he would have been able to afford a retirement in which he had to “manage” monthly distributions for the last 3+ decades and hopefully more to come.

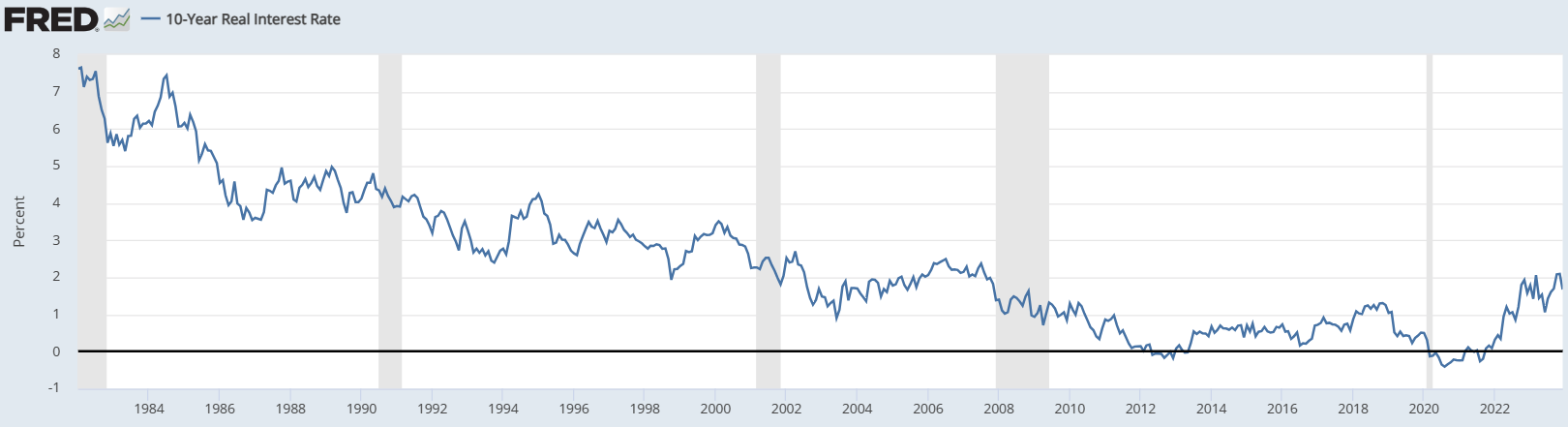

The higher US interest rate environment has reduced the present value (PV) of those future value (FV) benefit payments promised by sponsors of DB plans to their plan participants. Perhaps this development will encourage plan sponsors to maintain, if not reopen, their DB plan. The current American retirement landscape is not good, and it will only continue to get worse, as members of younger cohorts (Millennials, Gen X, and Gen Z) move along toward their retirement age. Unfortunately, these generations have been burdened with greater expenses associated with education, childcare, and housing affordability. Funding a retirement account becomes such a secondary consideration to just being able to make ends meet.