I am very thankful to Asset.tv for once again having me on to discuss the Butch Lewis Act. They remain incredibly supportive in feeding information regarding this potential landmark legislation to their audience. Here is my latest interview with Sarah Makuta.

It’s Not The ROA

The WSJ’s Heather Gillers wrote an article in today’s edition titled, “Pension Funds Still Making Promises They Probably Can’t Keep”. Always glad to see pension plans get some air time in the WSJ, but would really appreciate a new slant on what is truly happening.

As always, the theme of the article is the “failure” on the part of Pension America to achieve the proverbial Holy Grail return on asset assumption (ROA). As many of you know, defined benefit (DB) plans used to be managed against their liabilities, and quite effectively. There are many reasons why this changed, but I would assign a fairly significant role to the advent of the asset consulting community, who in trying to justify their existence created a sea change that had plan sponsors seeking return, and naturally, the ROA was pursued at any cost.

Meeting the promise (benefits) at the lowest cost possible had been a very successful strategy. The dramatic shift from low cost to high return has created the funding nightmare that was addressed in the WSJ article. Unfortunately, the problem is even worse than what was articulated, as GASB allows public and multiemployer plans to discount liabilities at the ROA, and not the AA Corporate rate used by corporate pension plans (FASB). This masking of the true liability shortchanges these plans each year, as contributions don’t match what should actually be deposited.

There are several strategies that should be used by plan sponsors that would help get these plans back on a stronger footing that isn’t dependent on generating a return that exceeds the ROA objective. DB plans need to be preserved for the masses, as asking untrained workers to fund, manage, and disperse a retirement benefit through a DC plan is just poor public policy.

Perhaps POBs Should Be Revisited

“Some state and city governments have turned to pension obligation bonds (POBs) to pay their unfunded liabilities in their pension programs, and Moody’s lists these bonds as a part of the net tax-supported debt. However, the Government Finance Officers Association advises against issuing these bonds at all because they carry significant risks, both for the investor buying them and for the government issuing them.”

The above quote appeared earlier this week in a ValueWorks article, by Michelle Jones, titled, “State Debt Burdens Are Improving, But Pension Situation Only Getting Worse”. We won’t argue with the fact that many of the POBs issued earlier this century have not provided the benefit that was expected. Why? Unfortunately, most plan sponsors and their consultants put the proceeds from the bonds into a traditional asset allocation hoping to achieve an arbitrage between the forecasted return on asset assumption (ROA) and the interest rate on the loan. This is the wrong strategy!

POBs are not an inappropriate pension financing tool provided that proceeds are used to de-risk the pension system instead of injecting greater risk as they have done in the past. We would recommend that any pension system planning to use a POB would adopt the alpha/beta approach that KCS and Ryan ALM have been espousing for years. We would highly recommend using the bond proceeds (beta assets) to defease the plan’s Retired Lives through a cash-matching strategy. The remainder of the assets (alpha assets) would be in a broadly diversified asset allocation excluding traditional fixed income, which is highly correlated to pension liabilities. The goal of the alpha assets is to beat liability growth and not the ROA.

By defeasing the plan’s Retired Lives, the system has secured the promised benefits in the near-term, improved liquidity to meet those benefit payments, converted a highly interest rate-sensitive fixed income allocation into a much lower risk strategy, and extended the investing horizon for the alpha assets to capture the liquidity premium that exists in these assets. As success is achieved in the alpha portfolio versus liability growth, transfer excess alpha assets to the beta portfolio further improving the plan’s risk profile.

POBs have been tainted by poor execution. Invested properly, these bonds can provide significant improvement to a plan’s funded status while reducing contribution volatility.

Contribution Growth Rate Falling for Public Pension Systems

Some good news to report for public pension systems (and those that contribute to them). Fitch Ratings has reported that after hitting a high of 8.6% growth in fiscal 2011, median actuarially determined contributions (ADC) rose only 3.5% in 2017. Actual contributions rose slightly faster at 3.7%, as governments continued to pay a marginally larger share of what actuaries targeted for supporting these pension systems.

Unfortunately, despite the recent trend, pension contribution growth has been far faster than the growth in state and local tax resources, according to Fitch. State and local tax revenues (resources) are greater by roughly 33% during the last decade, while pension ADCs are 74% higher. Obviously, this differential in growth is not sustainable.

There is some concern being expressed that future contributions will have to rise as asset returns fall short of return on asset (ROA) objectives, while demographic shifts reduce employee contributions. We, too, are concerned about plans injecting too much risk into their investment structure and asset allocation decisions that might exacerbate funding volatility.

As we’ve stated on numerous occasions, just because GASB allows public and multi-employer pension systems to discount liabilities at the ROA doesn’t make it a prudent action. Furthermore, it hides that fact that the present value of future liability payments can fall as interest rates rise. But, those only discounting liabilities at the “fixed” ROA would not recognize that fact.

Sure, pension systems might fall shy of their return objective (median ROA target is 7.5%) during the next decade, but if liability growth is actually negative, does it matter? Public pension systems would benefit from a greater understanding of what their promise looks like (benefit payments) and use that output to drive future asset allocation decisions. As funded ratios improve, plans should de-risk. With a de-risking glide path in place, contribution volatility should be reduced as well.

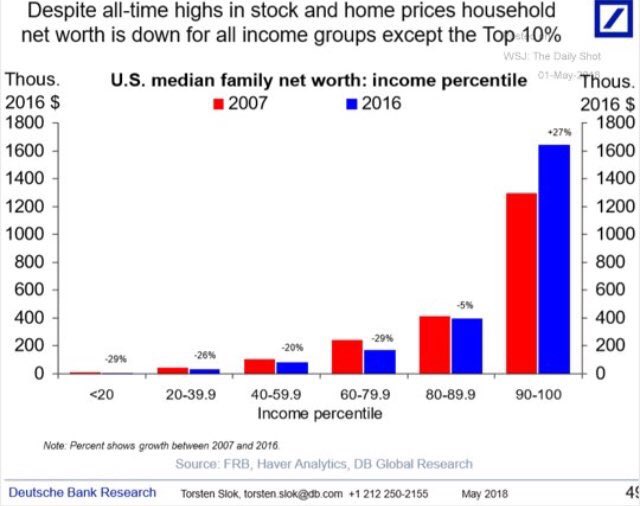

How Have the Significant Stock Market and Housing Gains Impacted You?

If you are fortunate enough to be in the Top 10% of income then you’ve done fairly well since the GFC. However, median family net worth for all but the Top 10% have fallen in the last decade. As we’ve pointed out before, 84% of the stock is owned by just 10% of the American population. Corporate share buybacks provide a disproportionate benefit to a small percentage of Americans.

A Trend Worth Following For Public Pension Plans

“For the 69 U.S. corporate sponsors that participated in the CEM database in 2007 and 2008, the average decline in funded status over 2008 was 30%,” the analysis points out. “A quarter of the plans saw declines in excess of 37%, and fewer than 10% of plans remained fully funded on a U.S. GAAP basis at the end of 2008. Despite the relatively positive returns for many asset classes in recent years, the decline in interest rates has proven to be a large impediment to restoring the funded status of pension plans to pre-crisis levels.”

According to CEM’s study, the predominant investment theme among U.S. corporate plan sponsors has been to risk reduction, “both on an asset-only basis and also more importantly, with reference to their liabilities.”

One investment concept that has gained prominence is the de-risking glide path, a process by which a plan’s strategic asset allocation is gradually reduced, as either funded status improves, interest rates increase, or both. “Thirty percent of U.S. corporate sponsors in CEM’s database stated that they had a formal de-risking glide path in place at the end of 2016.”

Another point being stressed in the study is the fact that “a fixed-income allocation is not a perfect proxy for LDI investing, as it does not capture the duration of the fixed income investments in relation to liabilities.” We, at KCS and Ryan ALM, couldn’t agree more, which is why we recommend adopting a defeasement strategy that cash-matches retired lives from nearest to as far out as possible.

Taking risk off the table, as the plan’s funded status improves is a most prudent tool. Why continue to subject the plan to unreasonable risk of a potential 2007-2009 repeat when the average plans funded status declined by >30%? By reducing the chance that the public plan’s funded status will plummet, contribution expenses should be more consistent and less impactful on the greater social safety net provided by states and municipalities.

Plan sponsors have made a promise to their participants. Not knowing what that promise looks like on a regular basis is inappropriate, as it is this insight that should drive asset allocation and investment structure decisions.

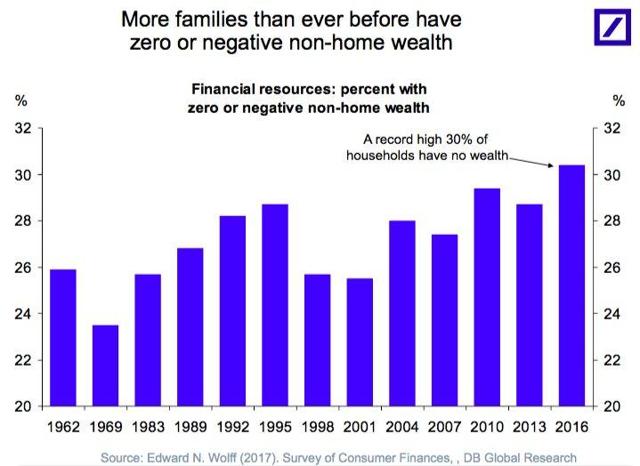

Another Picture, Another 1,000 Words

And if that chart isn’t enough to scare you, how about this one?

Joint Select Committee on Solvency of Multiemployer Pension Plans

Important legislation is being developed/debated in Washington DC related to protecting and preserving “Critical and Declining” multi-employer defined benefit plans and the PBGC in the process. Regular readers of the KCS blog know that we have been actively involved in supporting and presenting the Butch Lewis Act as the legislation best suited to accomplish this objective.

For those of you involved in the retirement industry, this Joint Select Committee will have an impact on the funds and participants that we serve, but also the service providers, too. Consultants, actuaries, investment managers, custodians, trading desks, data providers, etc. could see a major reduction in the number of DB plans if legislation isn’t passed that preserves these critically important plans.

We would encourage you to reach out to your legislators regarding the Butch Lewis Act. Encourage them to support the creation of Federal legislation that would provide low-cost loans to these nearly insolvent plans that would go a long way to preserving the promised benefits.

Here is a link to the official Joint Select Committee website. One can find information on the 16 members, news clips, documents, and hearings.

Joint Select Committee on Solvency of Multiemployer Pension Plans

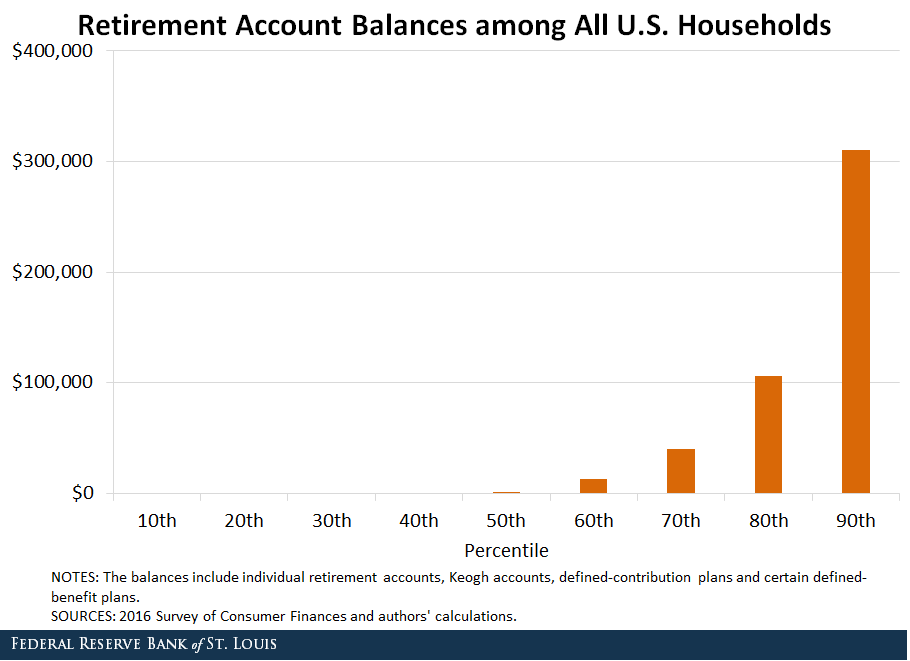

The median U.S. household has only $1,100 in retirement account savings

We recently reported that the average Senior spends $46,000 annually in retirement while incurring out of pocket medical expenses of $276,000. Something has to give!

Senator Brown Speaks on Need For Pension Protection

Here is a link to a recent presentation/video by Senator Sherrod Brown on the importance of protecting the pensions of workers in “Critical and Declining” multi-employer pension plans. The economic impact of our failure to protect these plans and their beneficiaries will be felt by everyone – not just the workers themselves! It is way past time talking about the retirement crisis. Something needs to be done right now, and adopting the Butch Lewis Act as law would be a great way to begin.