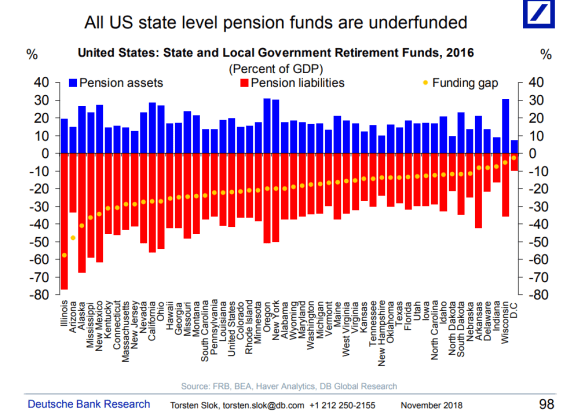

When KCS was established in August 2011, the mission of the firm was pretty simple. We set out to “help plan sponsors and their participants address today’s retirement plan challenges.” I can’t think of a greater challenge than the one facing the Critical and Declining multiemployer pension systems (roughly 114 plans) that badly need our help. Without a path forward these plans will face insolvency within a relatively short timeframe (<15 years) and the participants who are depending on the retirement benefits will likely see very little of the promise that they were given and helped to fund! UNACCEPTABLE!

The following article was shared with me through our KCS Facebook page. It is another attempt on the part of industry participants to claim that taxpayer-funded support of these critically important funds is inappropriate.

The short article version of Saving the PBGC, at the expense of the Pensioner. “Lawmakers should resist calls for taxpayers to bail out troubled pension plans with direct subsidies or “loans” from the federal Treasury, whether provided directly to pension plans or funneled through the PBGC. Doing so would unfairly transfer responsibility for pension underfunding from plan trustees to taxpayers and would likely exacerbate existing underfunding.”….

The Butch Lewis Act legislation that is being considered among other proposals by the Joint Select Committee on Solvency of Multiemployer Pension Plans does call for low-interest rate LOANS to be made available to these C&D plans in order to stave off plan failures. Without this help, there is little that can be done to ward off insolvency thus casting aside millions of plan beneficiaries who were counting on these promised benefits and have had nothing to do with the current funding crisis. Do these so-called industry experts really believe that the taxpayers (including these participants) will not be asked to support to a greater extent the social safety net that would be expanded to now include all of these participants?

Providing low-interest rate loans will extend the life of these plans by 30-years! The proceeds from the loans must defease all of the currently retired lives and terminated vesteds ensuring that benefits accrued to date will, in fact, be paid! Furthermore, the investment horizon for the future liabilities has now been extended by decades raising the probability of success.

The Butch Lewis Act Team included wonderful actuaries from Cheiron who analyzed each of the 114 plans, and they determined that 111 of the 114 plans would be able to meet current and future obligations and pay back the loan without any assistance from the PBGC. Yes, there are 3 plans that still would need help, but the estimated support is roughly 33% of what it would be if all of the plans were to become insolvent. Furthermore, the CBO has recently indicated that their analysis has the total loan program at only $34 billion, which is substantially lower than previous estimates.

If one were to add up the anticipated loan expense and the PBGC assistance, the $57 billion is roughly $11 billion less than the amount the PBGC would be on the hook for should each of the 114 plans fail. Furthermore, it is estimated that the plan participants receiving benefits generate nearly $1.1 trillion in annual economic activity. Can our economy survive an economic hit such as that? Where is common sense?

There have definitely been mistakes made along the way that have negatively impacted these pension systems. Allowing these pension plans to fail because of these issues is foolish. The Butch Lewis Act mandates that these pension systems operate in a more effective way, which will improve the likelihood of success. What could be wrong with extending the life of these plans by thirty years? Think about how many participants will be helped during that timeframe. The taxpayer should embrace this lifeline. It keeps them from having to support the participants within the next few years!

National Retirement Security Week is a national effort to raise public awareness about the importance of saving for retirement. National Retirement Security Week is held every year during the third week of October (it is October 21-27 this year). The week provides an opportunity for employees to reflect on their personal retirement goals and determine if they are on target to reach those goals.

National Retirement Security Week is a national effort to raise public awareness about the importance of saving for retirement. National Retirement Security Week is held every year during the third week of October (it is October 21-27 this year). The week provides an opportunity for employees to reflect on their personal retirement goals and determine if they are on target to reach those goals.