By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Yesterday, I produced the chart below with the intent to write a piece regarding premature recessionary fears. My premise was based on the fact that since 1970, recessions only occurred as unemployment rose/peaked. With today’s jobs report, I am more convinced that we will be saddled with inflationary pressures for longer without a corresponding recessionary environment. The calendar year 2000 is interesting as unemployment began to rise but given the low level of unemployment at that time, the economy never went into recession. Could our current landscape be foretelling a similar outcome?

Produced by Russ Kamp, Ryan ALM, Inc.

As for today’s news, it’s been reported that US employers added a robust 528,000 workers in the last month which far exceeds prognostications by a factor of 2Xs. Furthermore, these new jobs spanned many industries/sectors. As a result, the unemployment rate now stands at 3.5%, which is the lowest level of unemployment in the last 50 years. As has been reported numerous times, individual balance sheets have been improved since the flood of government stimulus beginning in 2020. Their spending may be shifting from goods to services, but they are spending nonetheless!

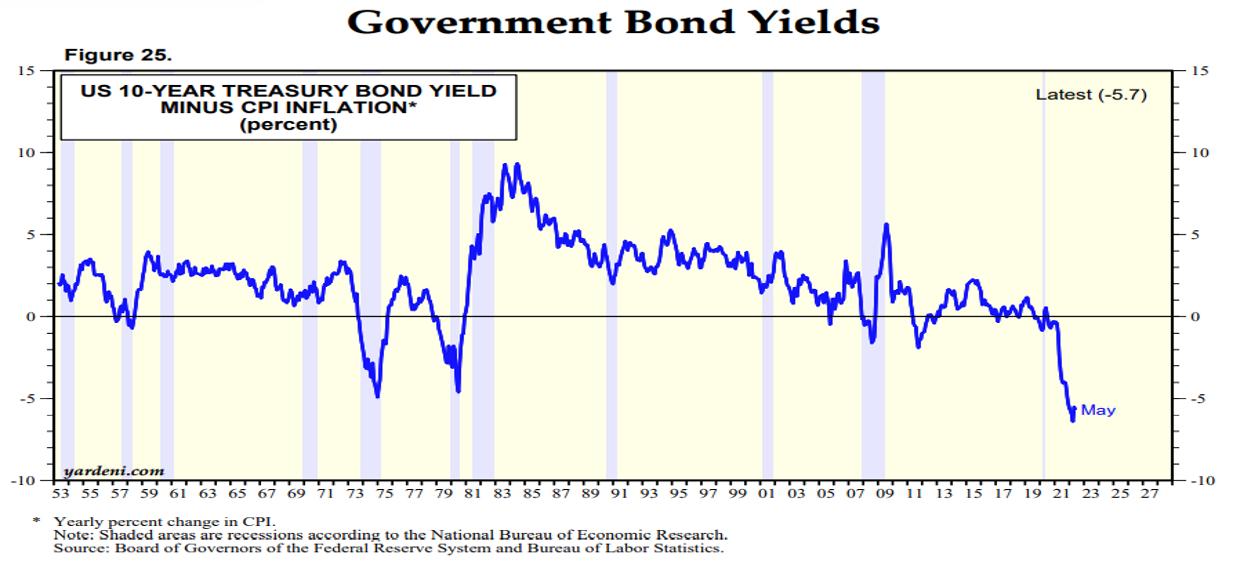

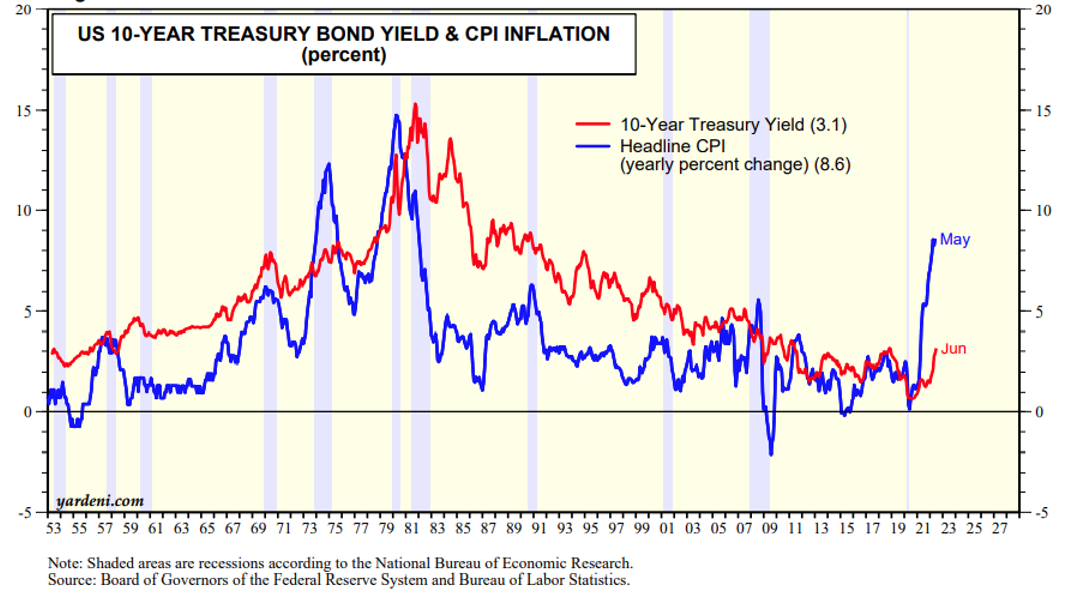

Bond investors that were anticipating a dramatic reversal in both inflation and interest rates may want to rethink that strategy given this news. As we’ve been reporting, US real rates are at historic lows providing “investors” with significant real losses after inflation. This news shouldn’t come as a shock. The US Federal Reserve has been showing its hand for quite some time that it would do what is necessary to tame the inflationary beast. We warned you on several occasions to not ignore the Fed. Caveat emptor!