We’ve been stating for a while that the unfolding U.S. retirement crisis would not only create a social and economic issue for individuals but that it would likely impact U.S. states, as well. We’ve just stumbled across an article in Employee Benefit Adviser written by Paula Aven Gladych, titled “Pennsylvania Focuses on Retirees Who Can not Afford to Retire”.

The article highlights the economic impact on Pennsylvania’s budget from increased expenditures to support the elderly population. According to Joe Torsella, PA State Treasurer, “when people don’t save enough for retirement, the states have to pick up the slack in long-term care and Medicaid and Medicare costs and state budgets get messed up trying to allocate enough funds to handle these extra charges”.

Pennsylvania decided to commission a study to look at its demographics and its ever-growing population of retirement age people. “As we suspected, there are significant impacts to state finances going forward from the state of our retirement preparedness,” Torsella says.

According to the article, “in 2015, Pennsylvania spent $4.25 billion in assistance costs for elderly residents. Fifty-four percent of this cost was attributed to the 21% of the elderly population who have $20,000 or less in annual household income, according to the report.”

If the elderly had been better prepared for retirement, meaning that they could replace roughly 70% of pre-retirement income, the state would have likely saved about $700 million in state assistance costs. The net impact of state assistance costs due to insufficient retirement readiness is likely to exceed $1 billion in the next 12 years.

We know that many small employers do not offer their employees a retirement program. We also know that employees are not likely to save outside of an employer-sponsored plan. Thus, it is imperative for states to begin to offer state-sponsored retirement programs that can offer payroll deduction to these small employers and their employees.

As the social safety net gets more expensive, tax hikes are likely to follow. There is a great chance that well-heeled residents will seek to live in less expensive states. We have already witnessed a significant exodus from Illinois to nearby states. If not careful, we could easily see this happen to other “Blue” states that have been impacted by recent Federal tax changes impacting one’s ability to deduct “SALT” taxes.

Finally, without a decent retirement benefit to rely upon residents won’t have the financial wherewithal to remain active participants in their economy. This will also negatively impact tax collections, businesses, and ultimately that state’s labor force. It is truly a vicious cycle.

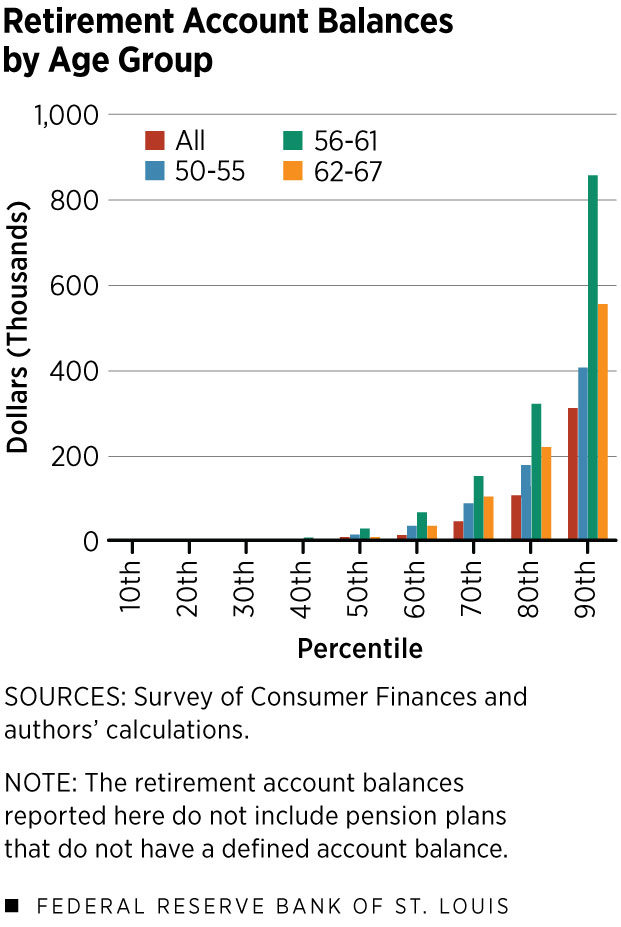

As one can clearly see, no near-retirement income group is in great shape when it comes to funding a retirement account, but the bottom 50% of older income earners are in terrible shape.

As one can clearly see, no near-retirement income group is in great shape when it comes to funding a retirement account, but the bottom 50% of older income earners are in terrible shape.