As those who regularly follow the Ryan ALM Inc. blog know, we report each week on the status of the PBGC’s effort to implement the ARPA legislation for multiemployer plans. In those updates, we have been reporting that the apparent slowdown in the processing of the special financial assistance (SFA) applications had to do with incorrect population surveys funds that have filed applications and in some circumstances have received SFA payouts.

We are finally starting to get some clarity on the situation in terms of who is involved and what is required of the funds that have received excess SFA grant money. In the most notable example, Central States, Southeast & Southwest Areas Pension Plan (CS) which received $35.8 billion in SFA in December 2022, has been informed that an excess SFA payment of $127 million was granted. This was the result of including 3,479 deceased participants in the eligible population. As a result, CS is required to repay the excess grant proceeds.

According to the Department of Labor, there are no consequences for those plans that have received excess grant money provided that they return those funds. According to a ai-cio.com article, “the DOL noted that this mistake was not made by the pension plan.” Unfortunately, the PBGC did not use the Social Security Administration’s death master file (DMF), a database that pension plans can’t access, when initially auditing SFA applications. They have since begun to use the DMF as of November 2023. “While these excess payment amounts may represent only a small fraction of total SFA payments, they would not otherwise have been paid and, as such, must be refunded to the United States government,” the PBGC said in a statement.

We hope that you enjoyed your St. Patty’s Day weekend.

Here is your weekly ARPA update on the progress of the PBGC as it implements the legislation. Last week saw a little action. Importantly, Employers’ – Warehousemen’s Pension Plan and American Federation of Musicians and Employers’ Pension Plan each filed revised applications. The Warehousemen’s plan, a non-priority group member, is seeking just over $40 million in SFA for its 1,821 plan participants. The AFM, a Priority Group 6 member, is seeking $1.44 billion for its nearly 50k members. The PBGC has 120 days to respond to these applications although I suspect that the necessary timeframe to evaluate the worthiness of the SFA applications will be shorter due to previous submissions.

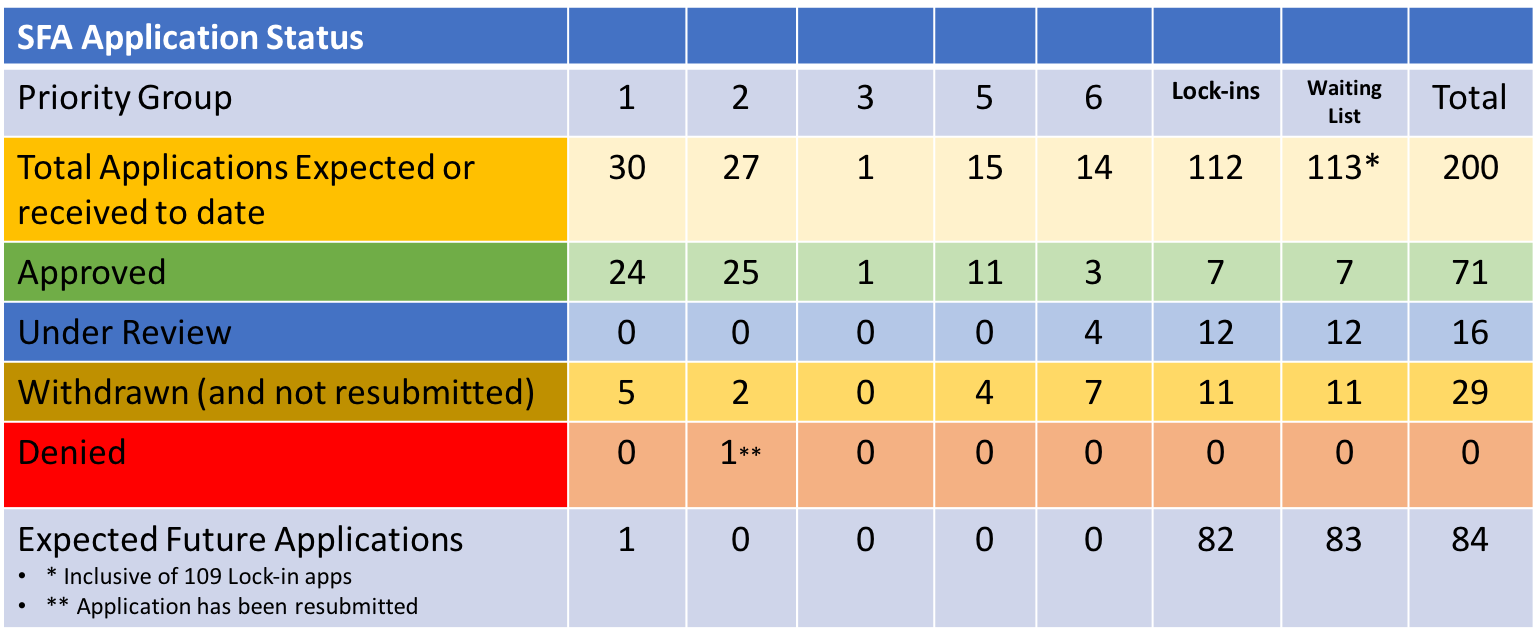

In other news, there were no applications denied, approved, or withdrawn, but there was an additional plan added to the waitlist, which now #s 113 members, although 27 have been submitted to the PBGC through their portal. The newest addition to the waiting list is PMPS-ILA Pension Trust Fund. They have elected not to lock in their valuation date at this time.

The US Treasury rate environment continues to rise from fourth quarter 2023’s bond rally. The increase in yields will allow for some greater cost reduction, and thus a longer coverage period for future benefits, for plan’s looking to defease those liabilities through a cash flow matching strategy. Since the beginning of 2024, the Treasury yield curve has shifted up about 40 bps for each key rate. As positive as this trend is for those looking to cash flow match, active, return-seeking fixed income products will have generated losses, especially for those with a longer duration objective. As a reminder, a portfolio with a 10-year duration will have lost about 4% in principal value.

The Milliman organization does a terrific of providing frequent and very useful updates through their Milliman 100 Pension Funding Index (PFI). They are reporting that the funded status improved by $26 billion in February for the largest 100 corporate defined benefit pension plans. The funded status at the end of February sat at 104.9% up from 102.8% at the end of January 2024.

All of the improvement in the funded status is the result of a higher discount rate that reduced the present value of those future pension promises. Unlike public pension plans, corporate accounting uses a AA corporate rate to value liabilities and not the ROA. Assets don’t need to rise in order for pension funds to show improvement in the funded status. In fact, during the month, Milliman estimates that liabilities fell in value by $30 billion. The current funding surplus for the members of this index stands at $63 billion at month end.

What’s next for these companies? Much of Corporate America has already begun to de-risk their plans. For those that haven’t the time is now to consider taking some risk out of the asset allocation. We certainly don’t want to see a repeat from 1999, when pensions were well over-funded on to see that funded status deteriorate rapidly with the advent of two major equity market declines. Importantly, de-risking doesn’t mean getting out of the pension game. it does mean that you, as the sponsor, don’t want to continue to ride the asset allocation rollercoaster up and down which can impact contribution expenses.

Migrate your fixed income from a return-seeking mandate to one that is now going to use bond cash flows of interest and principal to match the liability benefit payments. In an uncertain environment as to the direction of US interest rates, utilizing a cash flow matching (CFM) strategy will lock up the relationship with those pesky liabilities and eliminate interest rate risk for that portion of the portfolio. How comforting is that?

March has certainly blown in like a lion, especially on the east coast, where we’ve been living under wind advisors for the last few days. Fortunately, those haven’t been headwinds and as a result, the capital markets continue to be supportive of our retirement industry.

With regard to ARPA and the PBGC’s effort to provide Special Financial Assistance (SFA) to worthy and eligible multiemployer plans, the process has definitely slowed. In an email exchange with the sponsor of a fund that has recently had to withdraw their application, it was shared that the “death audit” being conducted by the PBGC on each of the applications has contributed to the slowing of the process. Hopefully, those plans that haven’t filed yet will go to the trouble of ensuring that the plan populations are accurate.

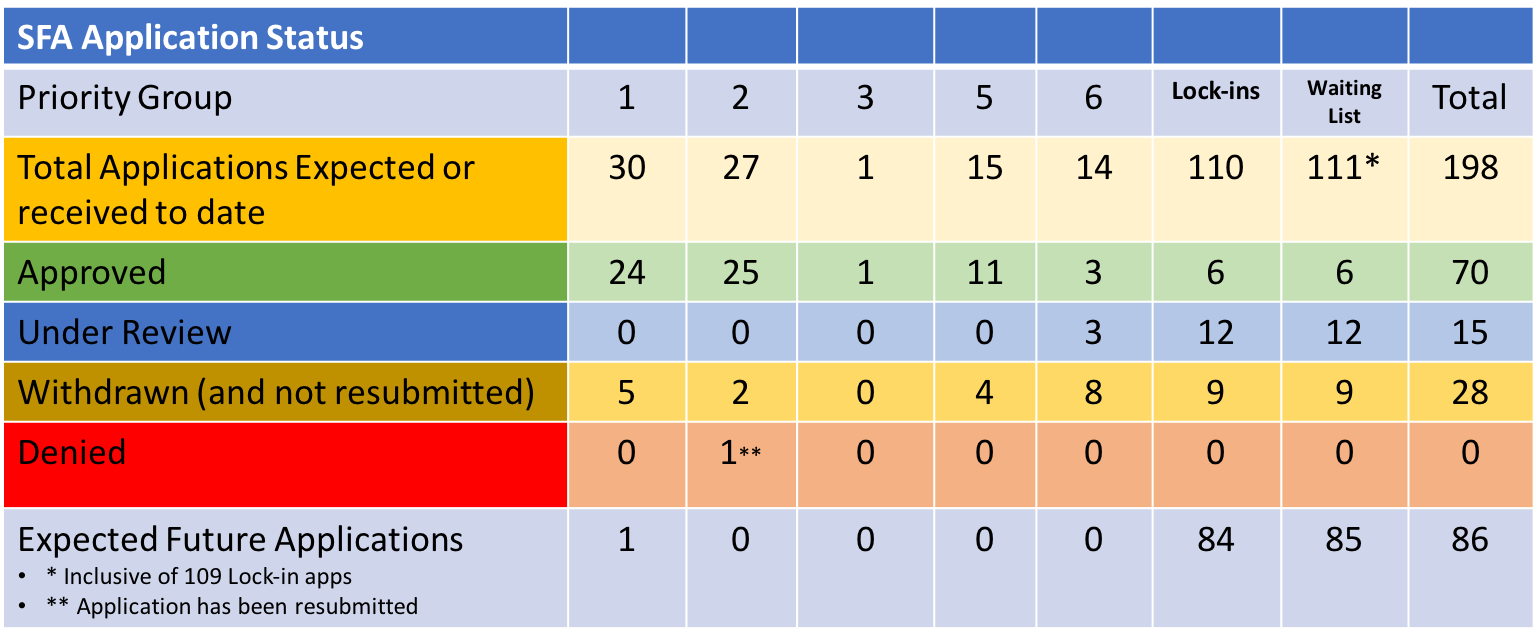

As far as the activity for the week ending 3/8, the PBGC has reported that no new applications were filed. Furthermore, none were rejected and there were no new withdrawals. We are pleased to report that one fund, Teamsters Union Local No. 73 Pension Plan, a non-priority group member, has had its application approved for $7.5 million in SFA for the plan’s 529 members.

As the chart above highlights, with 71 application approvals, the PBGC is 35.5% of its way through the current roster of potential SFA recipients. Much more to come!

I suspect that some (perhaps) many folks in our industry are becoming a little tired of my constant drum beat requesting a change in how pension plans are managed. I’m sorry if that is the case, but I have a reason to speak out often, if not loudly. My goal/mission, and that of Ryan ALM, Inc., is to protect and preserve defined benefit plans for the masses. I believe wholeheartedly that DB plans are superior to any other retirement program since they provide the monthly promise with little involvement from the participant, who may have particularly wonderful skills used in their day-to-day lives, but investing isn’t likely one of them.

By espousing Cash Flow Matching (CFM) as an important investment strategy, particularly in this period of attractive interest rates, we are bringing pension management generally and asset allocation strategies specifically back to its roots. The SECURING of the pension promise must be the primary objective for plan fiduciaries. Better yet, it should be accomplished at a reasonable cost and with prudent risk. As I’ve discussed before, a CFM strategy brings an element of certainty to the management of pensions that have embraced uncertainty through asset allocation strategies that are subject to the whims of the markets.

The riding of the asset allocation rollercoaster in pursuit of a performance objective does little to secure the pension promise, but it certainly adds to annual volatility of both the funded status and contribution expenses. Is that the outcome that the sponsors of these plans and the participants want? Heck no! Are we at Ryan ALM tilting at or own windmills? I sure hope not.

I’ve been heartened recently to read several articles favoring a return to pension basics, including the focus on the pension promise to drive asset allocation through a CFM implementation. I’m not afraid to be a lone wolf, and nearly 1,400 blog posts support that claim, but it is comforting to have some company, as being a contrarian outside of the “herd” has been described as being as painful as chewing off one’s left arm – OUCH! In one specific instance, Stephen Campisi, recently posted his article on LinkedIn.com, in which he espoused a similar bifurcated approach – liquidity and growth buckets – to pension asset allocation. He also reminded everyone that “aiming” at the correct objective was essential. In this case, he correctly cited that the objective was the promise that had been given to the participant.

Nothing would please me more than to have the entire industry once again realize the significant importance of the defined benefit plan and its role in securing a dignified retirement. Eliminating the rollercoaster cycles of performance will go a long way to preserving their use. Adopting a CFM strategy that secures the monthly promises at a reasonable cost and with prudent risk is the first step in the process. I look forward to you jumping on our bandwagon.

There has been much written during the last week about the current state of the US retirement industry. This follows testimony in Washington DC that highlighted many of the current issues related to retirement security or lack thereof. One of the statistics that grabbed my attention is the fact that >50% of Americans aged 65-years-old or older are “living” on <$30,000/year. That is as disheartening a fact as I’ve ever seen.

Where in the US can one afford to live on such a meager annual sum? Worse, without Social Security roughly 38% of the senior population would be living below the poverty line, that is currently (2024) defined by the Department of Health and Human services for all contiguous 48 states, Puerto Rico, the District of Columbia and all U.S. territories, at $15,060 (one-person household). It goes all the way up to a whopping $20,440 if you are fortunate to have a life partner living with you. Again, how can most live on this meager sum?

Social Security currently pays an average annual sum of just $21,384/year or just $1,782/month. Given that the average monthly housing rental is $1,372, that doesn’t leave one much for food, transportation, healthcare, insurance, or even TV viewing since everything these days is a pay-to-watch service, and that happens only after you’ve had to pay for the internet! One can almost forget about staying in their house, since property taxes continue to ratchet higher and higher, especially if you live almost anywhere on the East coast. For instance, the average property tax in NJ is now roughly $8,600/year with many communities seeing double and triple those rates.

This lack of income in retirement is forcing a larger percentage of those 65-years-old and up to seek employment in their “golden years”. According to AARP, some 20% of the Senior population is now gainfully employed. That figure was 10% in 1985. If you are fortunate to work in a white collar job, the opportunities are more plentiful. However, for those that have spent a lifetime engaged in more physical labor you can almost forget about participating during your sunset years.

I’ve written chapter and verse about the demise of defined benefit plans and the impact that trend was going to have on the average American worker. The use of DC plans in lieu of DB plans is poor policy. It isn’t working. The average American is not saving nearly enough to replace a meaningful portion of their income in retirement. This is and will continue to be a major source of concern as it has long-term implications for the states in which they reside. The social safety net that will be used to support these individuals with housing, medical, food, transportation, and other daily needs is already stretched. “A 2023 Pew Charitable Trusts study suggests that as more households with older Americans become financially vulnerable from 2021 to 2040, state governments will take a $1.3 trillion hit.” (Business Insider)

The retirement industry is in poor shape. Others will suggest that it isn’t, but the facts don’t lie. Too few Americans have access to a retirement account – there is not an age group that has participation at >60% – and for those that do, too many are not able to contribute a meaningful and appropriate sum. The lack of a crystal ball to help determine longevity and investment acumen combine to make managing one’s “retirement” more challenging. Please let’s stop pretending that it doesn’t.

Welcome to March. It is said that the weather in the Northeast comes in like a lion and exits like a lamb. Is the same true for markets? Given a lot of the crosscurrents in the markets from geopolitical concerns, equity valuations, AI, interest rates, and Fed policy, who knows what is in store for us this month and beyond.

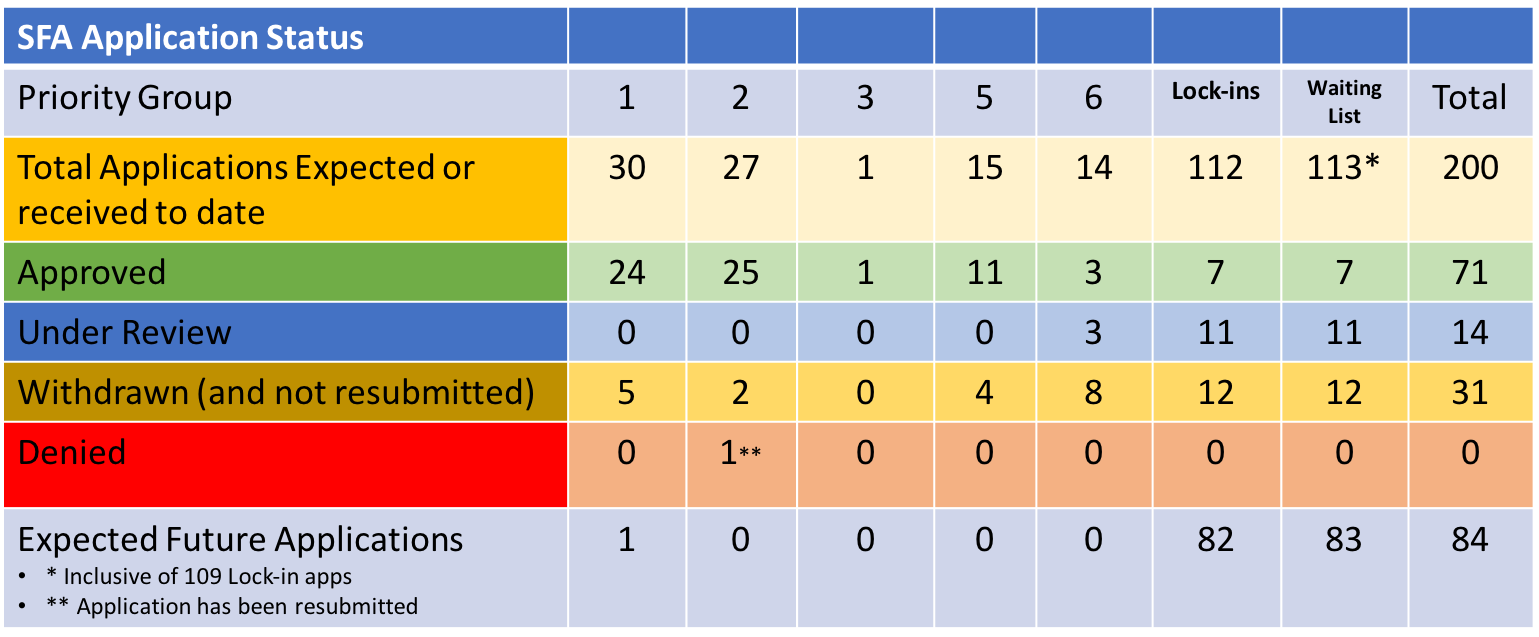

That said, we can with near certainty discuss what transpired during the last week as it relates to ARPA and the PBGC’s implementation of that critical legislation. I say with near certainty only because the weekly updated spreadsheet provided by the PBGC didn’t have a couple of actions from 2/23/24 that were only added in the March 1st update. Specifically, Union de Tronquistas de Puerto Rico Local 901 Pension Plan, a Priority Group 1 member, has once again withdrawn its application. They are seeking >$37 million for the 4,029 participants. In other delayed news, the American Federation of Musicians and Employers’ Pension Plan, a much larger fund and a Priority Group 6 member, has also withdrawn its revised application. They are in pursuit of an SFA grant that would provide the fund with $1.44 billion in SFA plus interest for more than 49k participants.

Now that we are caught up, this past week (ending 3/1/24) saw some activity, too. Two members from the waiting list entered their applications through the PBGC’s portal, including the Kansas Construction Trades Open End Pension Trust Fund and the Pacific Coast Shipyards Pension Plan. Both plans have submitted revised applications. Kansas Construction is seeking $40.7 million for its 8,145 participants, while the Shipyards plan is striving for $17.8 million for 507 participants, which is 35,108/participant compared to the roughly $5,000/participant for the Kansas plan.

In other ARPA news, there were no applications approved or denied during the previous week. There was one application withdrawn (2/26), but the Pacific Coast Shipyards quickly resubmitted the application by 3/1. In somewhat surprising news, there is a late arrival to the waitlist – # 113! Plasterers Local Union No. 1 Pension Plan joined the list on 2/26/24. They have also locked in the valuation date of November 30, 2023.

Have a great week. In the meantime, please don’t hesitate to reach out to us if we can be of any assistance to you as it relates to this legislation.

ESG, short for environmental, social, and governance, are considerations alongside financial investment insights used in investment decision making. ESG considerations have been around for a long time, and in most instances, they were prohibitions on the purchase of a particular investment. I recall early in my career a social issue not to invest in South Africa. This was followed by tobacco-free, sin stock-free, and many other imposed limitations on a variety of industries and sectors.

Today, the primary motivation in considering ESG factors is the idea of sustainability. What initiatives should a company take to ensure that their business will not only survive, but thrive, in the future. I’m not going to get into the politics surrounding ESG, but I do agree that sustainability should be a consideration in any investment. However, it shouldn’t be limited to the investment management community. Defined benefit pension plans should operate with the goal of being sustainable. I produced a post many years ago (01/2017) titled, “Perpetual Doesn’t Mean Sustainable“ in which I implored Pension America to rethink the approach to pension management.

Most, if not all, states, cities, and municipalities believe that they are perpetual, and they are correct, but it doesn’t mean that the funding of their public pension fund is sustainable, if the cost to administer the plan becomes onerous for the sponsoring entity. We’ve certainly witnessed the freezing of DB plans within the public sector, and it could continue to happen if changes aren’t adopted. I frequently rail about the traditional approach to asset allocation that has 100% of DB plan asset bases on a rollercoaster ride to reach an ROA target in which they ride markets up and then down only to basically stay in place from a funding standpoint – but contribution expenses certainly don’t!

If plans really want to become sustainable, and we certainly need them to be, they need to adopt as their primary objective the securing of the promises that have been given to their plan participants. Riding the rollercoaster in pursuit of a return objective has only ensured volatility of the funded ratio and contribution expenses. It hasn’t guaranteed success in meeting the objective, which is the securing of the benefits at a reasonable cost and with prudent risk. Why do plan sponsors continue to pursue a return objective and all the volatility surrounding that pursuit when there are strategies that can be used, for at least a portion, if not all, of the assets, that would bring certainty to the process of managing pension plans. A sustainable approach, I might add.

I read a post from a friend of mine yesterday (thanks, Chris), in which he showed a chart from BofA Research that looked at the price to normalized EPS for the S&P 500 over 10-year periods. BofA is forecasting a 3% per annum return for the 10-years ending 2034. Oh, wow! That isn’t going to help pension funding if it is anywhere close to reality. As the chart below suggests, the reality hasn’t been much different from the forecast.

So, what can plan sponsors do to make up for the potential shortfall? There is some great news. If you desire a more attractive return than a potential 3% per annum for the S&P 500, with all of the corresponding annual volatility, you can reallocate your bond exposure from a ROA return focus to a cash flow matching (CFM) mandate that will fund and match the plan’s liability cash flows. By securing the liabilities chronologically, you buy time for the residual (alpha) assets to grow unencumbered as they are no longer a source of liquidity. Importantly, once you match the asset cash flows (interest and principal) with the benefits (and expenses) you mitigate interest rate risk, while working to stabilize the funded status and contribution expenses.

Bringing some certainty to a very uncertain process is the ultimate in sustainability. Given how challenging many American workers are finding the management of a defined contribution offering, protecting and preserving defined benefit plans should be in everyone’s best interest.

Coalition Greenwich, a division of CRISIL, has released a report on the top trends in asset management for 2024. Among the categories discussed was the establishment of “Strategic Partnerships” among one’s clients. There were four categories in which 499 respondents to the survey were asked to rate from most influential when hiring an investment management organization to least influential. The categories included willingness to provide customization, fees, commitment to knowledge transfer, and finally brand recognition.

Not surprising, the willingness to provide customization achieved the top ranking in importance, with 72% indicating that it was either the most or very influential in the decision to bring on a manager and that product. We often read about a manager’s willingness to customize a solution, but what does that mean in reality? Ironically, Ron Ryan produced, just today, an article on the importance of creating custom liability indexes for LDI assignments. This was written primarily in response to a series of LDI-related research pieces that discussed “custom benchmarks” but used generic indexes.

In order to successfully implement an LDI strategy, especially one using Cash Flow Matching (CFM), the benchmark needs to be a custom solution that uses the client’s specific liabilities, as each pension plan has a unique set of liabilities, like snowflakes. The liabilities are future values that need to be priced at some discount rate(s) into present values (market values) similar to the plan’s assets. It is only then that an appropriate LDI strategy can be implemented.

Every client of Ryan ALM, Inc. gets a custom solution. There are no “off the shelf” products. Fees, which received the second highest ranking in importance, had 68% of the respondents rating this category as most or very influential. Despite the highly customized products, we at Ryan ALM, Inc. provide our services at low fees. We believe that the primary objective in managing a defined benefit plan is to SECURE the promised benefits at a reasonable cost and with prudent risk. Everything that we do as an investment firm is focused on that belief. Custom solutions and low fees – that doesn’t seem like the norm in our industry. We are proud to be different!

Milliman has once again provided perspective on the “average” public pension system with the release of the Public Pension Funding Index (PPFI), which analyzes data from the nation’s 100 largest public defined benefit plans. January’s result has the Milliman 100 PPFI funded ratio declining slightly from 78.2% at the end of 2023 to 77.7% as of January 31, 2024.

They attribute the decline to flat investment gains (-$11 million in market value), -$9 in net negative cash flow, and a slight increase (?) in the value of plan liabilities resulting in a change in funding by $33 million. The current funding gap of the index constituents is now -$1.4 trillion. But is that really what took place in January? We know that pension liabilities are bond-like in nature and move up and down with changes in US interest rates. The US rate environment changed quite a bit in January as yields moved higher across the US Treasury yield curve. Unfortunately, because most public plans are using their return on asset assumption (roughly 7%) to discount the plan’s liabilities, changes in interest rates are not reflected in the calculation of a plan’s liabilities.

How meaningful can the difference in accounting rules be among corporate and public plans? Just take a look at the Ryan ALM Pension Monitor for calendar year 2022, and you’ll note that the difference was substantial. In fact, both types of pension plans investing in the same markets, with reasonably similar asset allocations, had starkly different outcomes (a 32.1% difference!) as a result of the accounting rules used. Furthermore, Milliman reported that corporate plans actually showed improved fund ratios in January as a result of the discount rate change on plan liabilities. “The PFI projected benefit obligation, or pension liabilities, decreased to $1.316 trillion at the end of January 2024 from $1.337 trillion at the end of December 2023. The change resulted from an increase of 14 basis points in the monthly discount rate, to 5.14% for January from 5.00% for December 2023.” (Milliman)

Ron Ryan wrote an incredibly insightful book titled, “The US Pension Crisis” in which he placed appropriate blame on the accounting rules and the differences in how pension liabilities are calculated between FASB (corporate) and GASB (public) methodologies. Why these differences exist is beyond me, especially when one also understands that there exists a third methodology (IASB) that uses an even more conservative standard to measure a plan’s liabilities. Managing a pension plan is not easy, especially when the true value of a pension plan’s liabilities is unknown.

So, January was good for Corporate America’s pension funding, but bad for Public pension plans. With US interest rates having risen sharply since March 2022, the value of plan liabilities is closer to reality, but there still exists a gap today. It would be wonderful if the actuarial profession could agree on one methodology so that we didn’t get conflicting outcomes on an ongoing basis.