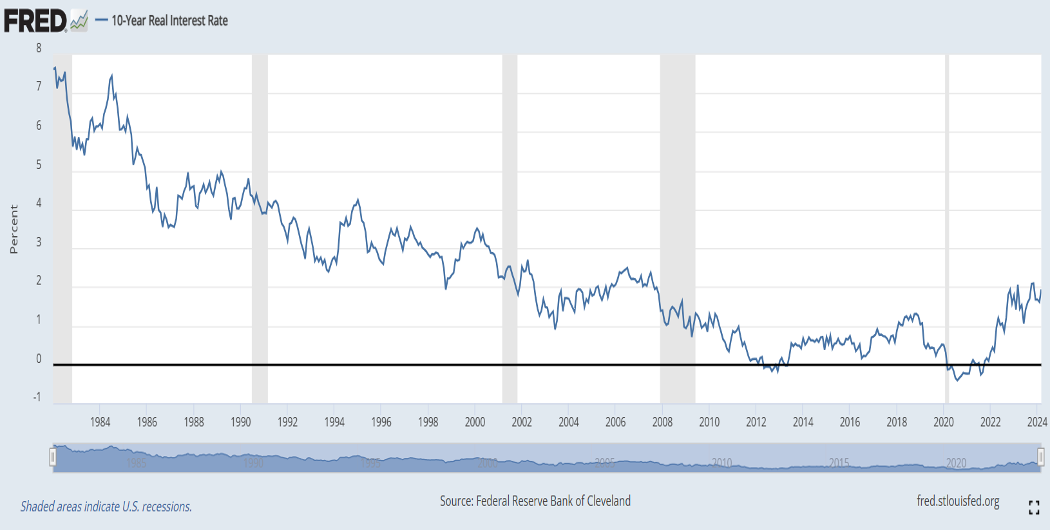

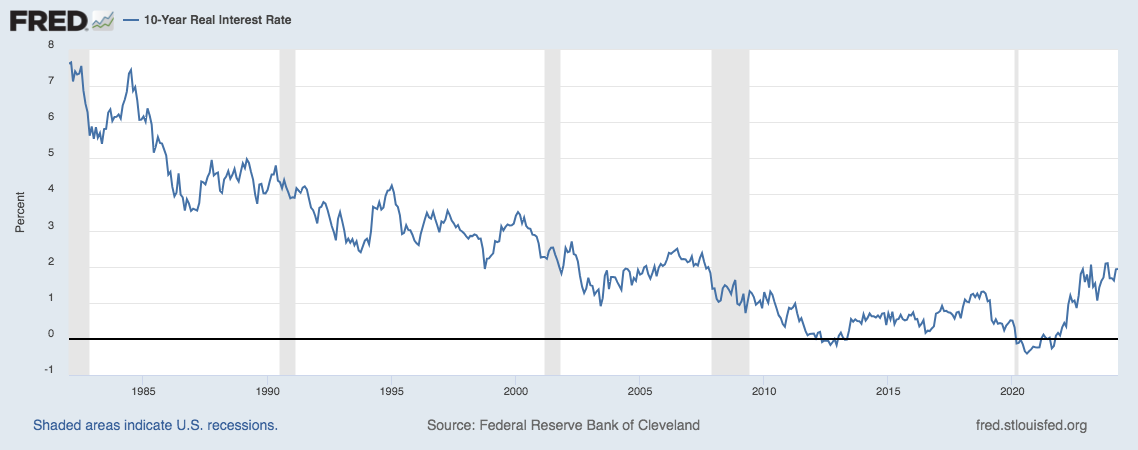

Chairman Powell and the Fed have consistently said they want real rates. The Fed primarily focuses on the Personal Consumption Expenditures (PCE) as their gauge of inflation. Currently the PCE is at 2.7%. What the Fed has not said is the target level of real rates. Historically, real rates as measured by the St. Louis Fed have averaged about 3.0% although the trend line has decreased steadily since the 1980s (see graph below). With the PCE at 2.7% today a 2% to 3% real rate would suggest a 4.70% to 5.70% 10-year Treasury nominal rate. With the 10-year Treasury at 4.66% today, it would seem that there is no reason for any cut in rates by the Fed. In fact, there may be more reason to increase rates.

The question remains… where will inflation (as measured by the PCE) level off? Who knows since there are too many factors to consider. The major causes of inflation today seem to be:

Excessive Government Spending

Biden 2025 budget of $7.3 trillion is 12.3% higher than the 2024 budget of $6.5 trillion. Jamie Dimon, CEO of JP Morgan Chase, warns that excessive deficit spending is inflationary and that interest rates could spike up to 8%. The Biden Administration Student Loan forgiveness package could increase the deficit by $430 billion if successful.

Oil Prices

West Texas Intermediate (WTI) Crude oil prices are up over 19% in 2024.

Red Sea Attacks

About 12% of global trade goes through here to the Suez Canal. Ships now have to be rerouted around southern tip of Africa creating a delay of about two weeks at a cost of $3,786 per vessel or about $1 million per week. According to Drewry World Container Index costs are up over 90% YoY.

Francis Scott Key Bridge Collapse

One of the largest ports in America handling $80 billion in cargo annually. Estimated closure costs = $15 million per day with closure expected for two to three years.

As always, the motto “let the buyer beware” (Caveat Emptor) seems to apply here.

Can you believe that a 1/3 of 2024 will soon be behind us? It is finally feeling like Spring in NJ today.

There is not much to discuss regarding the PBGC’s implementation of the ARPA pension legislation. According to the latest update, there were no new applications filed, approved, denied, or withdrawn. However, there was one fund that received the SFA. United Food and Commercial Workers Union Local 152 Retail Meat Pension Plan, a Mount Laurel, NJ, plan received SFA and interest in the amount of $279.3 million for the more than 10k plan participants.

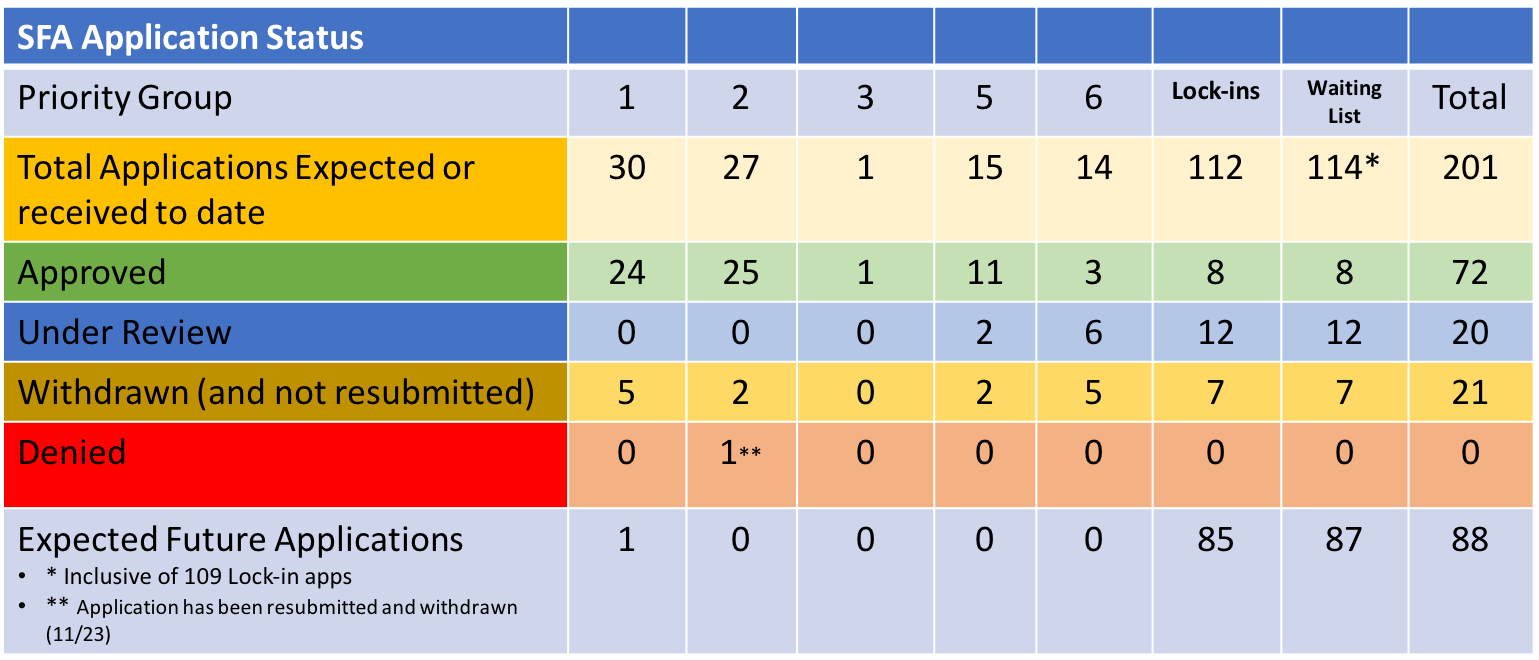

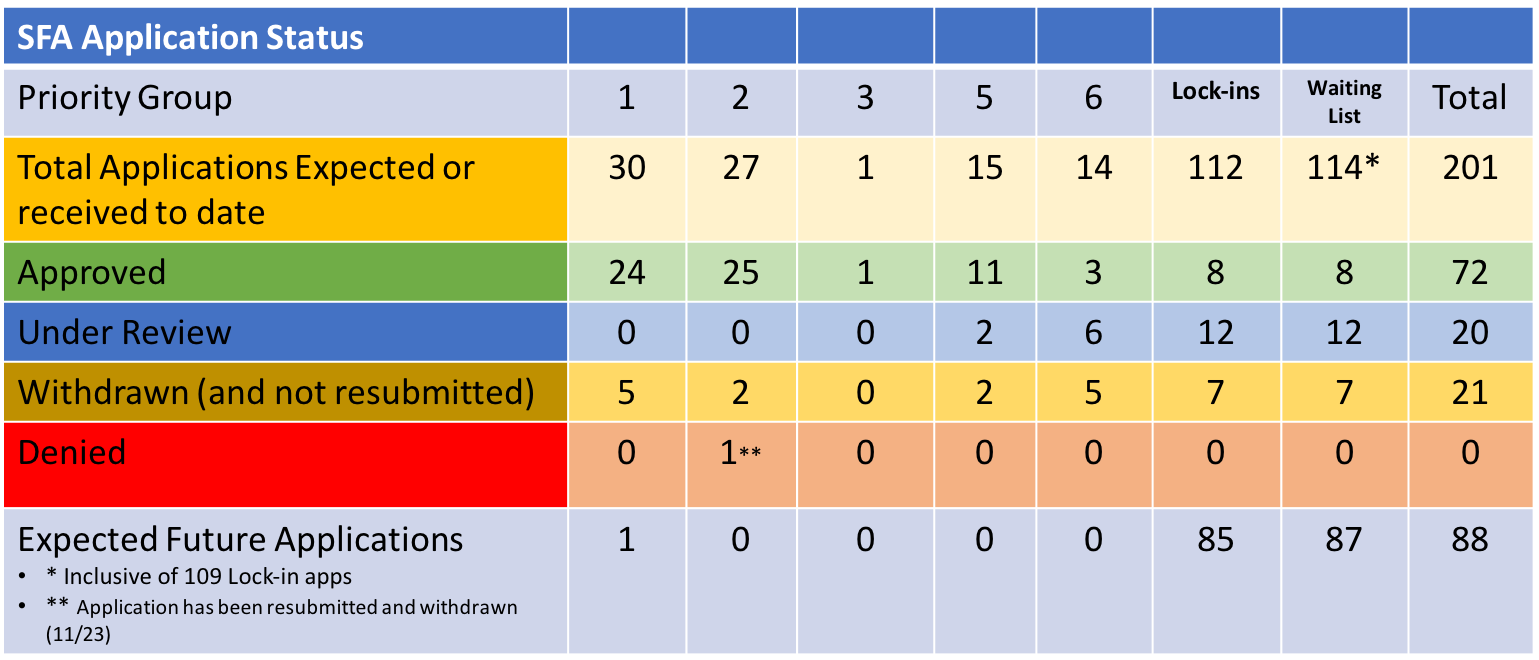

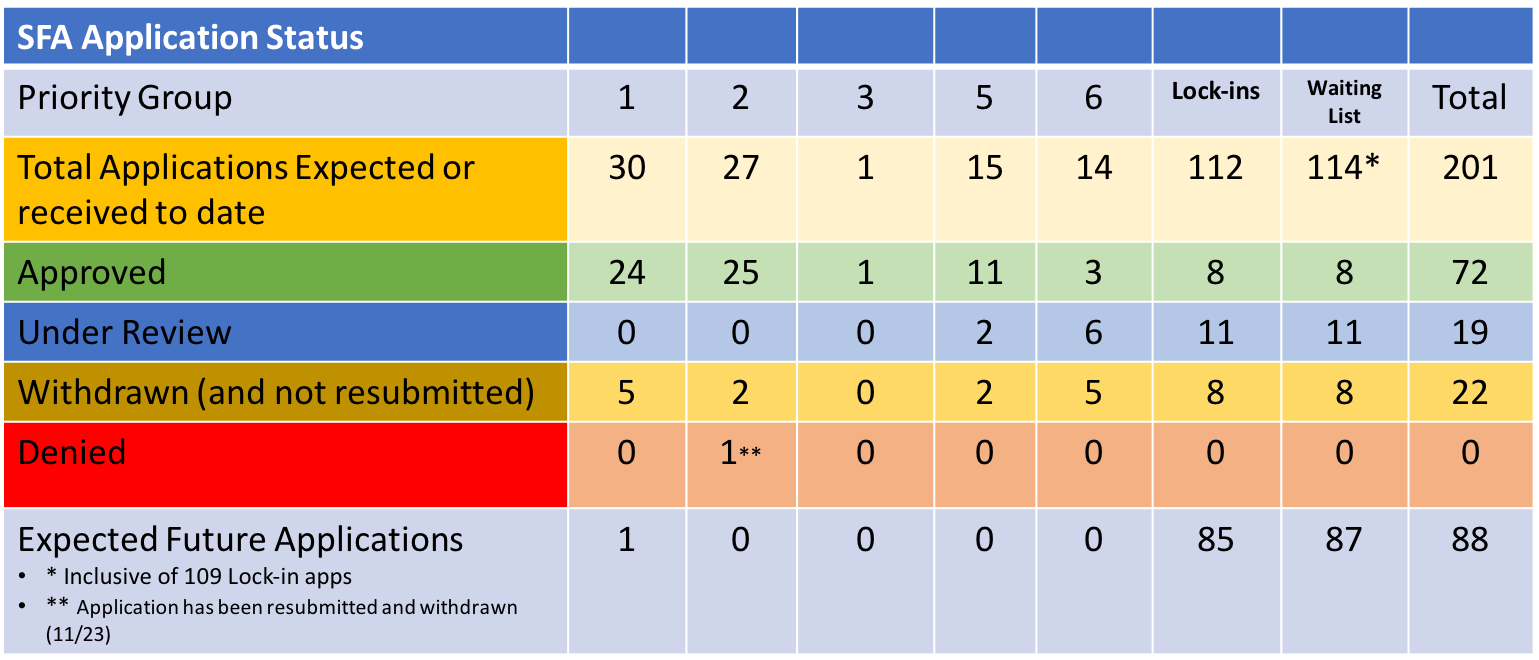

There currently are 114 names on the waitlist. Of those, 27 have been invited to submit applications. As the data above reflects, 8 of those applications have been approved, 12 are currently under review, while another 7 have been withdrawn presumably to have the submission corrected and resubmitted. In addition to that activity, 112 of the 114 funds have locked-in a valuation date for SFA measurement (discount rate). Ninety-two percent of those chose 12/31/22, while 2 have no lock-up and the other 9 have chosen dates between December 31, 2022 and November 30, 2023. As a reminder, the SFA is based on a series of discount rates. The lower the rate, the greater the potential SFA. Using the 10-year Treasury yield as a proxy for the discount rate, those plans locking in an evaluation date as of year-end 2022 have done alright, as the yield at the end of 2022 was 3.88%, while it currently stands at 4.63% (4/29 at 3:39 pm).

We’ll have to see if the others have faired as well. In the meantime, the higher US interest rates have certainly helped from an investment standpoint, as the current environment is providing 5%+ YTM investment grade bond portfolios. The higher rates reduce the cost of those future promises while extending the coverage period to secure benefits through a cash flow matching investment strategy.

Milliman recently released results for its Public Pension Funding Index (PPFI), which covers the nation’s 100 largest public defined benefit plans.

Positive equity market performance in March increased the Milliman 100 PPFI funded ratio from 78.6% at the end of February to 79.7% as of March 31, representing the highest level since March 31, 2022, prior to the Fed’s aggressive rate increases. The previous high-water mark stood at 82.7%. The improved funding for Milliman’s PPFI plans was driven by an estimated 1.7% aggregate return for March 2024. Total fund performance for these 100 public plans ranged from an estimated 0.9% to 2.6% for the month. As a result of the relatively strong performance, PPFI plans gained approximately $85 billion in MV in March. The asset growth was offset by negative cash flow amounting to about $9 billion. It is estimated that the current asset shortfall relative to accrued liabilities is about $1.271 trillion as of March 31.

In addition, it was reported that an additional 4 of the PPFI members had achieved a 90% or better funded status, while regrettably, 15 of the constituents remain at <60%. Given that changing US interest rates do not impact the calculation for pension liabilities under GASB accounting, the improvement in March’s collective funded status may be underreported, as US rates continued the upward trajectory begun as the calendar turned to 2024.

The WSJ produced an article on April 22, 2024 titled, “Path for 10-Year U.S. Treasury Yield to 5% Is Possible but Tricky” At the time of publication, the 10-year Treasury note yield was just under 4.7%. It is currently at 4.66%. Those providing commentary talked about the need to further reduce expectations for potential rate cuts of another 25 to 40 basis points. As you may recall, there were significantly greater forecasts of rate cuts at the beginning of 2024, but those have been scaled back in dramatic fashion.

Given the current inflationary landscape in which the Consumer Price Index for All Urban Consumers (CPI-U) increased 0.4 percent in March and 3.5% annually, a move toward 5% for the US 10-year Treasury note’s yield shouldn’t be surprising or tricky. According to the graph below, the US 10-year yield has averaged a “real” yield of nearly 2% (1.934%) since 1984. A 2% inflation premium would place today’s 10-year Treasury note yield at roughly 5.6%.

Given the current economic conditions (2.9% GDP growth for Q1’24) and labor market strength (3.8% unemployment rate), it certainly doesn’t seem like the Fed’s “aggressive” action elevating the Fed Funds Rate from 0 to 5.5% today has had the impact that was anticipated. Inflation in 2024 has been sticky and may in fact be increasing. Should geopolitical issues grow in magnitude, inflation may get worse. These current conditions don’t say to me that a move to a 5% 10-year Treasury note yield should be tricky at all. As a reminder, the yield on this note hit 4.99% in late October 2023. Financial conditions have not gotten more restrictive since then.

Should the Treasury yield curve ratchet higher, with the 10-year eventually eclipsing 5%, plan sponsors would have a wonderful opportunity to secure the future promised benefits at significantly reduced cost in present value terms, especially if the cash flow matching portfolio used investment grade corporate bonds with premium yields. Although US corporate bond spreads are tight relative to average spreads, they still provide a healthy premium. Don’t let this rate environment pass without taking some risk from your plan’s asset allocation. We’ve seen that scenario unfold before and the outcome is scary.

Welcome to the last full week of April. How is that possible?

There isn’t much to report from last week’s PBGC activity report, as only one event was reported. Retirement Benefit Plan of the Newspaper and Magazine Drivers, Chauffeurs and Handlers Union Local 473 (they have to win the award for the longest name), submitted an application last week seeking $29.7 million in SFA for the 804 plan participants. As a reminder, the PBGC has 120 days to act on this application before it is automatically approved. The Newspaper and Magazine Drivers fund is a non-priority fund that submitted a revised application.

I will be presenting Hot Topics in Investment Oversight at the Washington Legislative Update (IFEBP). This conference will address the key issues and players that are driving legislative and regulatory initiatives that impact your plans and plan participants. You can be sure that I will address ARPA and the positive impact that this legislation has had on an extraordinary number of American workers.

There appears in the WSJ today an article stating that pension plans were pulling “hundreds of billions from stocks”. According to a Goldman analyst, “pensions will unload $325 billion in stocks this year, up from $191 billion in 2023″. We are told that proceeds from these sales will flow to both bonds and alternatives. First question: What is this estimate based on? Are average allocations now above policy normal levels necessitating a rebalancing? Are bonds more attractive given recent movements in yields?

Yes, equities have continued to rally through 2024’s first quarter, and the S&P 500 established new highs before recently pulling back. Valuations seem stretched, but the same argument could have been made at the end of 2023. Furthermore, US interest rates were higher heading into 2023’s fourth quarter. If bond yields were an attractive alternative to owning equities, that would have seemed the time to rotate out of equities.

The combination of higher interest rates and equity valuations have helped Corporate America’s pensions achieve a higher funded status, and according to Milliman, the largest plans are now more than 105% funded. It makes sense that the sponsors of these plans would be rotating from equities into bonds to secure that funded status and the benefit promises. Hopefully, they have chosen to use a cash flow matching (CFM) strategy to accomplish the objective. Not surprisingly, public pension plans are taking a different approach. Instead of securing the benefits and stabilizing the plan’s funded status and contribution expenses by rotating into bonds, they are migrating both equities and bonds into more alternatives, which have been the recipients of a major asset rotation during the last 1-2 decades, as the focus there remains one of return. Is this wise?

I don’t know how much of that estimated $325 billion is being pulled from corporate versus public plans, but I would suggest that much of the alternative environment has already been overwhelmed by asset flows. I’ve witnessed this phenomenon many times in my more than 40 years in the business. We, as an industry, have the tendency to arbitrage away our own insights by capturing more assets than an asset class can naturally absorb. Furthermore, the migration of assets to alternatives impacts the liquidity available for plans to meet ongoing benefits and expenses. Should a market correction occur, and they often do, liquidity becomes hard to find. Forced sales in order to meet cash flow needs only serve to exacerbate price declines.

Pension plans should remember that they only exist to meet a promise that has been made to the participant. The objective should be to SECURE those promises at a reasonable cost and with prudent risk. It is not a return game. Asset allocation decisions should absolutely be driven by the plan’s funded status and ability to contribute. They shouldn’t be driven by the ROA. Remember that alternative investments are being made in the same investing environment as public equities and bonds. If market conditions aren’t supportive of the latter investments, why does it make sense to invest in alternatives? Is it the lack of transparency? Or the fact that the evaluation period is now 10 or more years? It surely isn’t because of the fees being paid to the managers of “alternative” products are so attractive.

Don’t continue to ride the asset allocation rollercoaster that only ensures volatility, not success! The 1990’s were a great decade that was followed by the ’00s, in which the S&P 500 produced a roughly 2% annualized return. The ’10s were terrific, but mainly because stocks were rebounding from the horrors of the previous decade. I don’t know what the 2020s will provide, but rarely do we have back-to-back above average performing decades. Yes, the ’90s followed a strong ’80s, but that was primarily fueled by rapidly declining interest rates. We don’t have that scenario at this time. Why assume the risk?

In the last 10 days or so, I’ve felt an earthquake in NJ, witnessed the eclipse in Dallas, and then saw the magnificence of a double rainbow on Saturday evening. What does Mother Nature have in store for me this week?

Fortunately, the PBGC didn’t have many surprises for us during the last week, as activity was mainly kept behind closed doors. They did provide an update on Friday, as they customarily do, but there wasn’t much to show. In fact, there were no new applications filed, approved, denied, or withdrawn. There was one new fund added to the waitlist. Pension Plan of International Union of Bricklayers & Allied Craftworkers Local #15 PA added its name to the list on April 10th. They became the 114th fund to be on the list. As previously reported, 27 of those have filed an application with 8 having been approved for an SFA grant.

There has been a new tab added to the PBGC’s weekly update, as a result of excess SFA grant money being repaid. The first fund to return excess grant money is the Central States, Southeast & Southwest Areas Pension Plan, which returned $126.7 million or 0.35% of the initial grant payment. They are the first, but they likely won’t be the last to have to do so.

Economic and labor market conditions remain positive, likely keeping US interest rates elevated in 2024. These higher rates provide SFA recipients with the wonderful opportunity to defease the promised benefits at lower present value cost. Let us help you!

Managing a pension plan should be all about securing the promised benefits at a reasonable cost and with prudent risk. I believe that most plan sponsors would agree, yet that is not how plans are managed, especially public and multiemployer plans that continue to pursue the return on asset assumption (ROA) as if it were the Holy Grail. I’ve written quite a bit on this subject, including discussing asset consulting reports that should have the relationship of plan assets to plan liabilities on page one of the quarterly performance reports.

We know that pension liabilities are like snowflakes, as there are no two pension liability streams that are the same given the unique characteristics of each labor force. Furthermore, most pension actuaries only produce an annual update making more frequent (monthly/quarterly) updates more challenging. Would plan sponsors want a more frequent view of the liabilities if they were available? I think that they would. Again, if securing the promised benefits are the primary objective when it comes to managing a pension plan, then plan sponsors need a more frequent view of the relationship between assets and liabilities.

Why is this important? First and foremost, the capital markets are constantly moving, and the changes impact the value of the plan’s assets all the time. But it isn’t just the asset-side that is being impacted, as liabilities are bond-like in nature and they change as interest rates change. We’ve highlighted this activity in both the Ryan ALM Pension Monitor and the Ryan ALM Quarterly Newsletter. However, accounting rules for both multiemployer and public plans allow a static discount rate equivalent to the plan’s ROA to be used that hides the impact of those changing interest rates on the value of a plan’s liabilities and funded status.

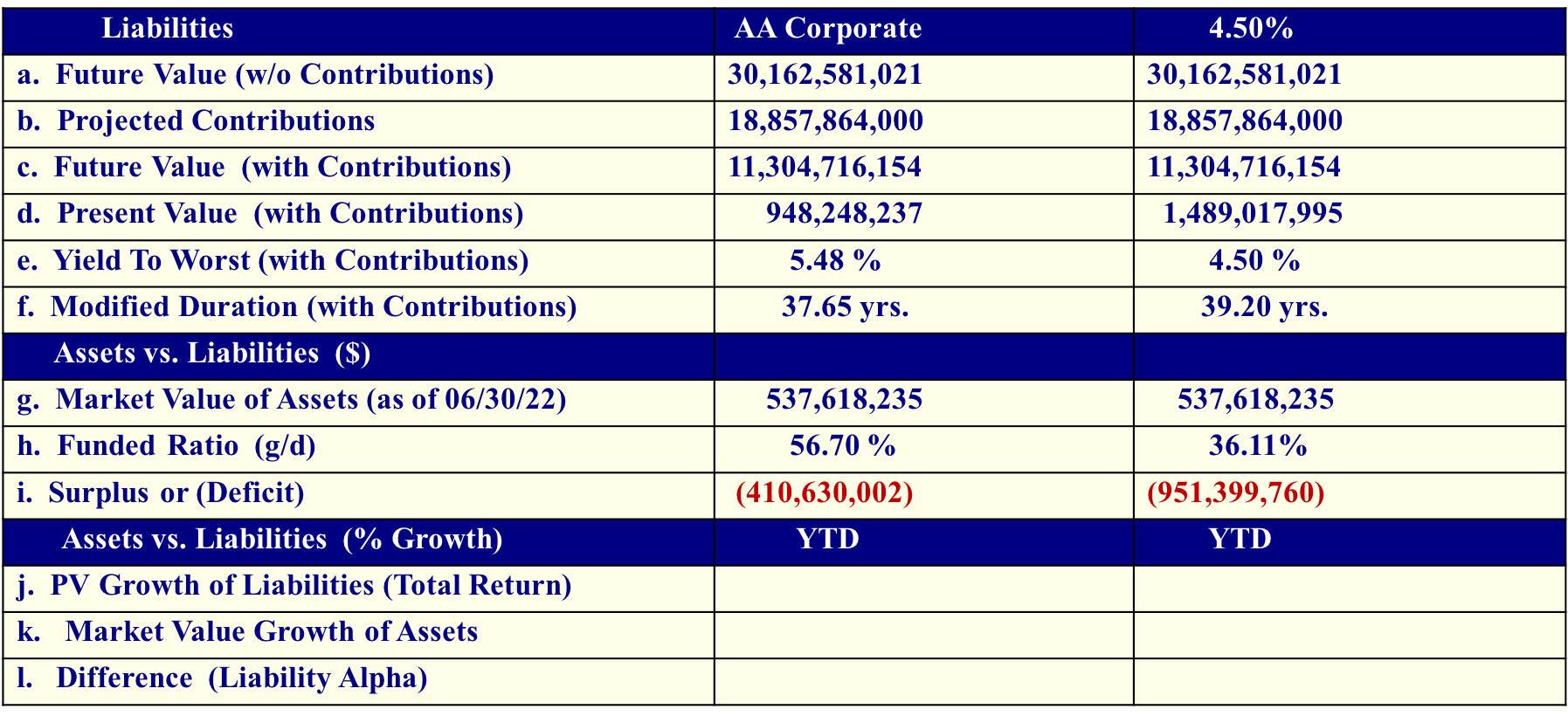

What if a more frequent analysis was available at a modest cost. Would plan sponsors want to see how the funded status was behaving? Would they want that comparison available to help with asset allocation changes, especially if it meant reducing risk as funding improved? I suspect that they would. Well, there is good news. Ryan ALM, Inc. created a Custom Liability Index (CLI) in 1991. The CLI is designed to be the proper benchmark for liability driven objectives. The CLI calculates the present value of liabilities based on numerous discount rates (ASC 715 (FAS 158), PPA – MAP 21, PPA – Spot Rates, GASB 67, Treasury STRIPS and the ROA). The CLI calculates the growth rate, summary statistics, and interest rate sensitivity as a series of monthly or quarterly reports depending on the client’s desired frequency.

The above information is for an actual client, who we’ve been providing a CLI for 15+ years. This client has elected to receive quarterly reviews. They’ve also chosen to see the impact on liabilities for multiple discount rates, including a constant 4.5% ROA, which could easily be a pension plan’s ROA of say 7%. As you will note, the present value (PV) of those future value (FV) liabilities are different, and they could be dramatic, depending on the interest rate used. In this case, the AA Corporate rate (5.48% YTW) produces a funded ratio of 56.7%, while the flat 4.5% rate increases the PV liabilities thus reducing the funded status by more than 20%.

Using Treasury STRIPS as the discount rate produces the lowest funded ratio of 33.7% or 23% lower than using the AA Corporate discount rate.

With this information, plan sponsors and their advisors (consultants and actuaries) can make informed decisions related to contributions and asset allocation. Most plan sponsors are currently blind to these facts. As a result, decisions may be taken without having all of the necessary facts. Pension plans need to be protected and preserved (Ryan ALM’s mission). Having a complete understanding of what those future promises look like is essential.

You’ve made a promise: measure it – monitor it – manage it – and SECURE it…

Get off the pension funding rollercoaster – sleep well!

We are pleased to provide you with the Ryan ALM, Inc. Q1’24 Newsletter. You’ll find lots of interesting information related to defined benefit pensions, with a particular focus on pension liabilities. The firs quarter of 2024 was a good quarter for pension America, as rising rates and strong asset gains combined to improve funded status for all plan types.

That said, there have been several recent articles that included comments from leading actuaries imploring plan sponsors to take risk out of their current asset allocations. We’ve encouraged pension plan sponsors to do that for decades, as riding the asset allocation rollercoaster has only lead to increased contribution expenses and volatility of the funded status. It is time to adopt a new approach. One that will secure the promised benefits and allow participants and plan sponsors to sleep better at night.

Please don’t hesitate to reach out to us if you’d like more information on how to de-risk a plan. We’ve written chapter and verse on the subject.

Welcome to ECLIPSE DAY. Good luck found me in Dallas today for the TexPERS conference, as it is in the path of totality (complete darkness). Bad luck has it heavily overcast today following a Sunday that had beautiful blue skies. Oh, well. Perhaps we’ll get lucky.

APRA’s implementation by the PBGC has slowed, and we don’t have earthquakes (NJ residents are still shaking their heads), eclipses, or any other natural event to blame. That is not to say that nothing has been done, as there was one new application received during the week. Printing Local 72 Industry Pension Plan, a Priority Group 5 member, submitted its revised application seeking $37 million in SFA for the 787 plan participants. Beyond that, I suspect that they are busy reviewing the 19 applications that have been submitted that are currently waiting on approval. Only 5 of those applications are the initial version.

As we’ve discussed in previous updates, census data used to determine SFA grant payments has had to be checked and rechecked following the announcement that Central States received more SFA grant $ than they were eligible to receive since some of the participants were no longer alive. That revelation and the corrective measures taken to ensure that SFA monies are only being allocated for eligible participants has really slowed an already cumbersome review. Despite some of these impediments, it is great that 72 plans have gotten the SFA awards totaling nearly $54 billion.

We might not have great visibility as it pertains to the eclipse, but with US interest rates tending higher, inflation remaining more “sticky” than hoped, and a Fed that may just not cut in 2024, visibility is clearer that cash flow matching the SFA is the way to secure the benefits and expenses well into the future. As a reminder, as rates rise, the cost to defease those promised benefits falls. Higher rates aren’t only good for savers. They are particularly good for SFA recipients and all plan sponsors of DB plans.

As an example of how that math works, when I entered this industry on October 13, 1981, the 10-year Treasury was yielding 14.9%. It would have only cost you $17.82 to defease a $1,000 30-year liability. On August 4, 2020, when the 10-year Treasury yield dipped to 0.52%, it would have cost you an extraordinary $860.40 to defease the same $1,000 30-year liability. As of April 5, 2024, the 10-year Treasury is yielding 4.41% and the cost to defease that 30-year liability is much more manageable at $301.00. You should be cheering for a higher for longer scenario.