By: Russ Kamp, Managing Director, Ryan ALM, Inc.

I’ve been fortunate to have participated in the investment/pension industry for more than four decades. I’ve seen the business from several perspectives, including as an asset/liability consultant and an investment manager. I’ve been involved in shops focused on equities, fixed income, and alternatives. I’ve also benefited from seeing the business through the lens of both fundamental and quantitative approaches. Lastly, I’ve worked at both large and small firms. As a student of our industry, I’ve learned a few things.

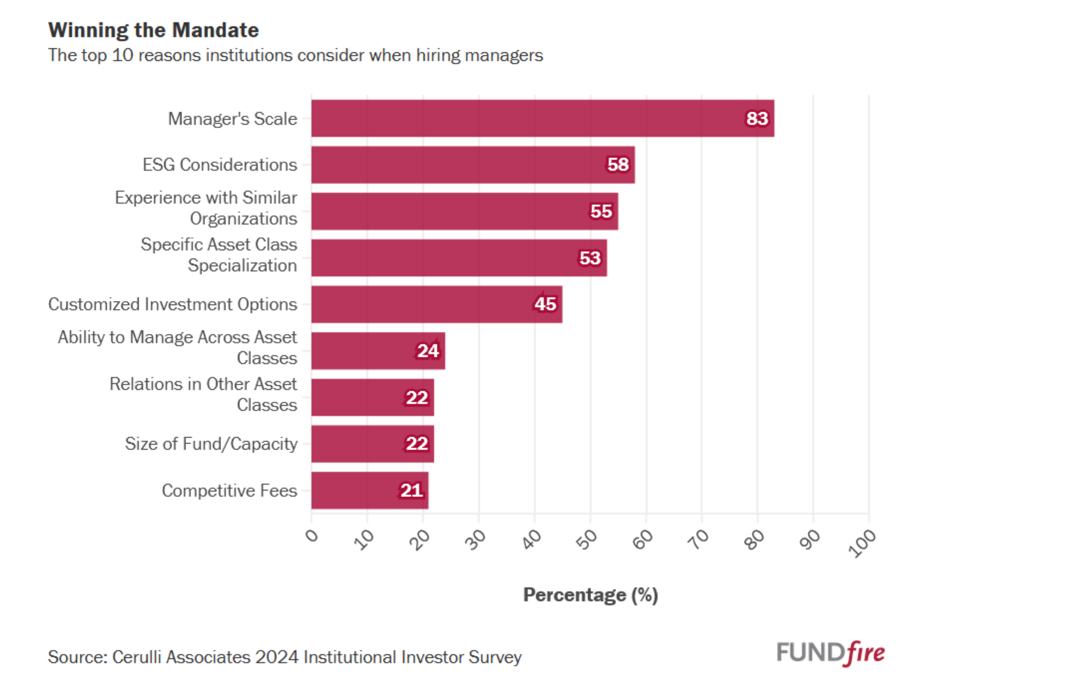

Based on my experience, having expertise in a particular investment discipline has always been the key to success. Another important data point in producing the desired outcomes is knowing when your AUMs have exceeded the natural capacity of that strategy. Yet, there seems to be this belief that size matters (scale). According to a recent article in FundFire, participants in the survey overwhelmingly indicated that scale was the most important characteristic in their hiring decision. Incredibly, specific asset class specialization was down at #4 with only 53% of respondents believing that was an important attribute. Seriously?

Our industry continues to “reward” larger firms, whether they be equity, fixed income, and/or alternative related with new mandates whether those firms actually add value or not. Importantly, there is only so much capacity within a single investment discipline, and our industry tends to overwhelm those capacity limits and the insights that are used. The quant crash in 2007 was brought about by having too much money chasing a few ideas. Those ideas got run over by the growth in the space. Insights can and did get arbitraged away by that AUM growth. This cycle of boom and bust is constantly being repeated, as we are seeing today with the loading up on products “investing” in anything AI-related. Yet, capacity is only a consideration for 22% of the participants.

Want to know why the average “active” investment manager isn’t adding any value? That firm has likely far exceeded the natural capacity in their strategy. Having the discipline to say “NO” to new mandates is not easy, but in the long run it is essential. Why potentially engage in an activity that might risk the entire franchise for the chance to bring in a few more $s? I recall limiting individual position size based on the percentage of a day’s trading volume. We constrained our exposure to <25% of the daily volume. At the same time, a larger competitor of ours had 34 days volume in the same stock. Try getting out of that stock without moving the market.

If I’m sitting in the plan sponsor’s chair, I am focused on three critical investment management attributes, and size (large) isn’t one of them. I would want to work with a firm that constantly evaluates the insights that they bring to their product to make sure that those insights are still adding value. If not, it is time to cast that idea aside and bring new insights to the table. I’d want to work with a firm that doesn’t push off the shelf product but can design a unique solution that meets my specific needs. Finally, I’d want to work with an investment management organization and not a sales shop. The true investment firm will understand just how much capacity there is in the strategy and they will do everything that they can to work within that restriction.