By: Russ Kamp, Managing Director, Ryan ALM, Inc.

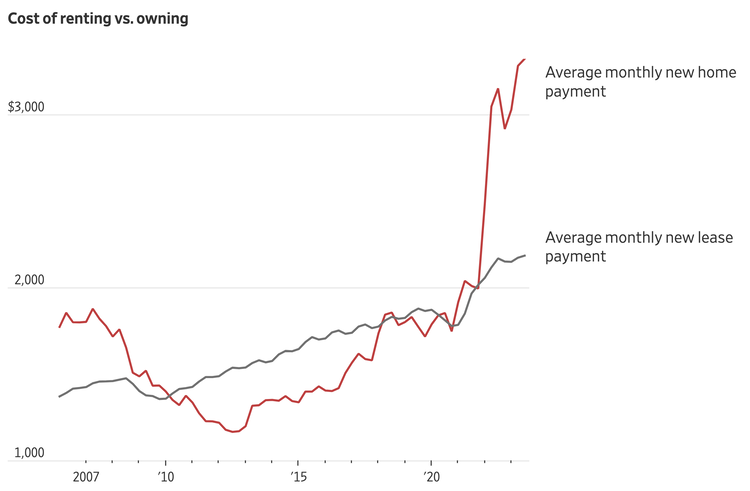

For most Americans buying a house has become nearly impossible, especially since the Fed’s aggressive rate increases beginning in March 2022. As the WSJ reported earlier today, and highlighted in the below graph, affordability has never been more challenging.

Mortgage rates have recently fallen to 7.6% (conventional 30-year) having peaked at 8.28% earlier this year. However, home prices have continued to rise, with the median house in the US hitting $392,000 in October, as supply of single family homes remains incredibly tight. In today’s environment, buying a $400,000 home with 20% down and mortgaging the balance over 30-years results in today’s purchaser incurring nearly $360,000 more in interest expense. In order for the new homeowner to keep their $2,000/month for housing budget intact, you’d have to find a house for about $295,000 or roughly $100,000 less than the current median cost. Good luck!

At the same time, working Americans are being asked to fund their retirements that employers once did. The combination of funding a defined contribution plan and trying to put a roof over one’s head is a math problem that many can’t solve. Many Americans are trying, but few have the financial means to fund at a level that will come close to providing a “benefit” that will replace 70% of their pre-retirement income for their golden years. This reality is why it is so critically important to have a retirement benefit that doesn’t rely on the individual worker to fund, manage, and then disburse the proceeds.

I’ve mentioned just two of the major expenses facing Americans. What about health insurance, student loan debt, property taxes (especially if you live in NJ), food, energy, clothing etc. Try buying a new car? Fortunately, we are at full employment (3.7% unemployment) and wage growth remains right around 4% annually. But is that enough to keep Americans housed and contributing to their retirement programs? I’m not sure and I really worry about the generations following the Boomers.