By: Russ Kamp, Managing Director, Ryan ALM, Inc.

Regular readers of this blog know that we’ve been on record since the first Fed Funds Rate increase that we were likely in a higher for longer scenario. That the prior nearly 40-year bull market for bonds was about to be eradicated, and with that would come pain for most investors who hadn’t worked and, in many cases, lived through a period of sustained inflation and rising rates.

One year ago, I published a post titled, “Tough August For Bonds“, which wasn’t referring to Barry Bonds once again being rejected by MLB’s Hall of Fame, although he was. At this point last year, the FOMC had elevated the FFR 5 times (which is now 11 times), and many investors were sure that US interest rates were nearing a peak. We didn’t think so, and expressed that sentiment with the following:

“Based on the current strong employment picture with 315,000 jobs created, 5.2% annual wage growth, and a labor participation rate that grew 0.3% in August (62.4%), it is likely that the Federal Reserve needs to continue to aggressively elevate rates until it accomplishes its primary objective of reducing inflation. This action will continue to weigh on the performance of the US bond market. Fed Chairman Powell has admitted that the Fed’s policy will inflict pain on American families as the strong labor market needs to be tamed. In order to impact the labor market, US rates must rise substantially. Are fixed-income managers and their clients prepared?“

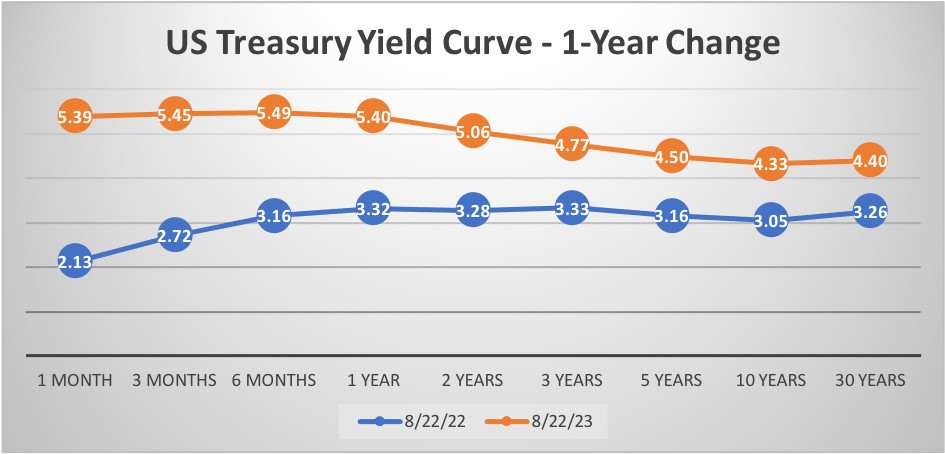

Based on the following graph, I guess that we were correct.

The Fed’s action has yet to inflict pain on the American family (fortunately) despite the aggressive increases in US rates, as the US labor market remains strong. These increases really haven’t inflicted much pain on the overall economy, as GDP growth has been well above consensus so far through two quarters and the third quarter is looking exceptional, if the Atlanta Fed’s GDPNow model is to be believed as they are forecasting a 5.8% annualized growth rate. Oh, my!

It isn’t hard to imagine that the Fed will once again say in September that inflation remains well-above the stated objective and that rates will be adjusted based on the data. For us, that means a scenario of higher for longer. If so, I must ask: Are fixed income managers and their clients prepared?

We didn’t have to wait until September, as Fed Chairman Powell delivered his speech in Jackson Hole, WY. Declares once again his commitment to getting inflation down to 2%. US Treasury yields rising across the curve.